One of the challenges with marketing is that there are so many bits that don’t fit together. As such let me put on record that I appreciate the potential for customers to be put at the center of all the marketing approaches. CLV, the value of a customer to the firm, has potential for a starring role in any unified theory of marketing. I am a believer in this. (Although not such a firm believer that I would like to have an inquisition to burn marketing heretics. Much though that would make American Marketing Association meetings a bit more dramatic.)

CLV As Customer Centric And Long Term

The advantage of using CLV as a central measure for marketers is that it is most obviously customer centric. It encourages firms to focus on the needs of the customer — given that is where the value to the firm is coming from. This is more aligned with marketing ideas than focusing on the product. CLV is also long-term. This gets us away from single-period measures that can be misleading and certainly tend to discourage investments in marketing. Sunil Gupta and Don Lehmann in a 2006 article make these points well.

CLV And Sunk Costs

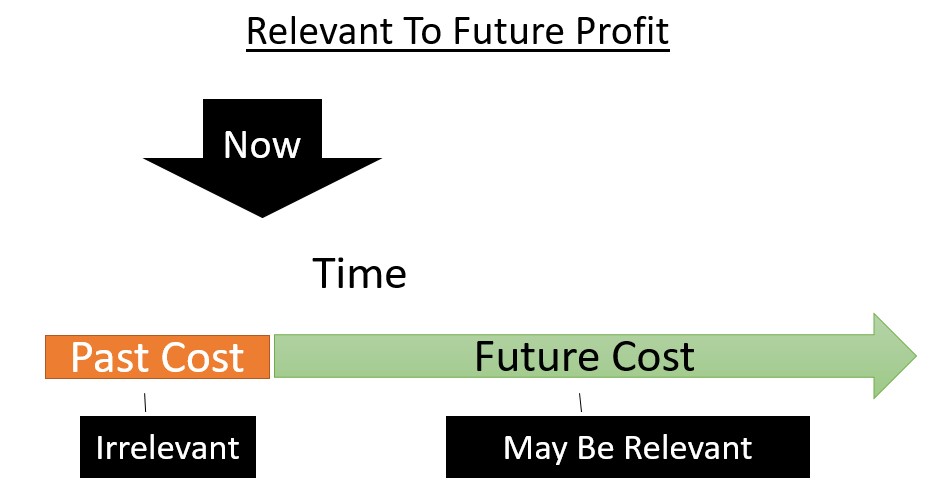

It wouldn’t be a CLV related post, though, if I didn’t complain about confusion around sunk costs. It is a central rule of good judgment that sunk costs absolutely should not be considered for decision making and yet this mistake is made all the time. Partly I think because we, academics, are not as consistent as we could be. The authors clearly tell us how to perform a CLV calculation:

CLV is the present value of all future profits obtained from a customer over his/her relationship with a firm.

Gupta and Lehmann, 2006, page 93

Sadly the metric they give immediately below subtracts acquisition costs (equation 2 in the paper). To be clear acquisition costs are a sunk cost for any current customers. As such, the equation does not represent the definition for current customers at least. The equation at most could only apply to future, i.e. non-customers, which is pretty odd for a customer lifetime value formula.

In equation 3 on the next page they drop the mention of acquisition costs. This is better to my mind but if CLV is to be central to marketing thinking we need to clearly define what CLV is. Still this work was pioneering so it is important to understand this is a side criticism of an important piece of work.

CLV And A Unified Theory Of Marketing

I wholeheartedly agree with the authors’ aims (which is why I worry that they are undermining their own aims).

The basic premise of this paper is that the concept of CLV is central to multiple constituencies.

Gupta and Lehmann, 2006, page 107

This is a crucial idea. This a key reason why we need define to CLV in a way that works for many different constituencies. To promote a unified theory CLV must work broadly. It cannot just be for acquisition marketers or those valuing future customers of the firm. Those assessing acquisitions don’t really need to worry about the sunk cost problem given all the money they spend on acquisition is at the very beginning of the process. This means it can’t be historically irrelevant — i.e. sunk.

As an aside, although acquisition costs clearly matter when assessing projected profit from future customers, such cost can be more transparently brought into consideration separately. As such, I would also argue that CLV, without subtracting acquisition costs, is still a better metric for acquisition marketers and corporate valuation. (Though I agree my argument here is less self-evident).

Tidying up our definitions we can certainly use CLV as a central point in our marketing theory. I will leave the authors the last positive word. We can work towards this.

Indeed, [CLV’s] power may well be in laying the groundwork for a “unified theory” of marketing which is relevant and understandable both inside and outside marketing.

Gupta and Lehmann, 2006, page 108

For more on CLV see here.

Read: Sunil Gupta and Donald R. Lehmann (2006) Customer Lifetime Value And Firm Valuation, Journal of Relationship Marketing, 5(2/3) pages 87-110