It is great that accountants are looking at the idea of valuing a firm through its customers. I very much welcome this. That said, I do worry that people bringing ideas from outside their field often bring back bad habits with them. (To be clear I am sure I do this when looking at non-marketing research). When I look at the work of Massimiliano Bonacchi and Paolo Perego I am filled with both excitement and concern. Excitement arises that accounting may take up the idea of customer accounting more seriously. Yet, I also have the concern that marketer’s bad habits might infect accounting or, more likely, mean accountants reject marketer’s good ideas because of the marketer’s bad habits. As such, I want to say ‘customer accounting, thanks but’.

Customer Accounting

The authors start nicely by laying out why it is useful to focus on customers. They outline a sensible definition of CLV but note that there is variety.

The work generally focuses on subscription-based enterprises which makes sense as the data is better there and the modeling easier. They also importantly point out the concept does apply more widely. The authors have a very clear view of what would be useful and a powerful call to action.

We further argue that companies should disclose in the Management Discussion and Analysis (M,D&A) section of their annual report a set of customer metrics useful to investors, such as new subscriber acquisitions, revenue per subscriber, customer dropouts, and cost of customer acquisition.

Bonacchii and Perego, 2019, page 10

This is all good stuff. There is much to admire in the approach and the fact that accountants are taking good ideas from marketing.

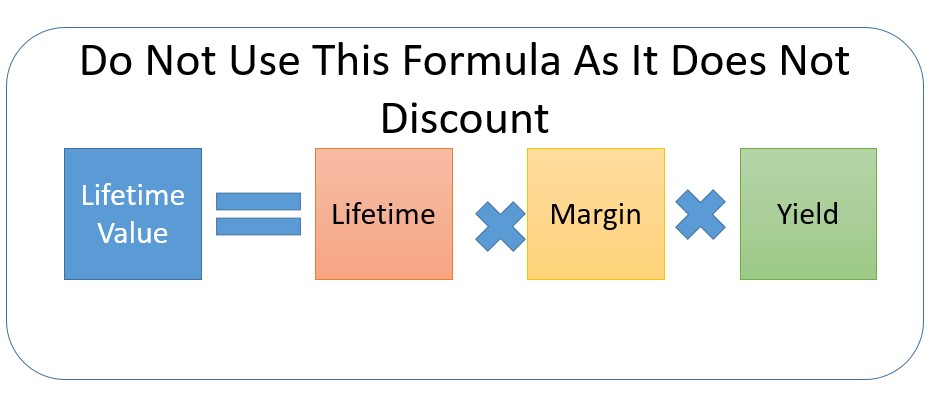

Customer Accounting, Thanks But What About Discounting

Then we run into some challenges. They are similar challenges to those I see in marketing. The problems are the sort of frustrating casualness with concepts. For example, one source of frustration is that they highlight a sensible definition of CLV that discounts to reflect the time value of money (page 16). Later they tell us a new equation that does not discount.

Their justification for not discounting includes a wonderful use of the passive voice (my emphasis). Clearly, someone believes that discounting is not needed but we aren’t sure who these villains are and we shouldn’t blame the authors. To be clear when I quote this it isn’t me that thinks discounting is optional.

In theory, the issue of the time value of money must also be considered, usually discounted in the CLV formula, in order to get an estimate of future profits. Discounting may be very appropriate in some businesses, particularly for firms operating in markets with a very long-cycle, high ticket retail and B2B. However, it is believed that the discounted practice may confuse the analysis in a B2C where the environment is very dynamic and it is better to adopt a simplified approach.

Bonacchi and Perego, 2019, footnote 6, page 22

They don’t give a proper reason for abandoning discounting. Basically, I think the sentence says that things change quickly in B2C. This implies that the future can’t be predicted. If true this means that predictions of the future don’t matter much. But if the future doesn’t matter then why use lifetime values? Such calculations only have a purpose when you need to consider the long term. (See more here.)

Simplify But Not To The Point It Doesn’t Make Sense

I fear Bonacchi and Perego had some marketing friends who told them that marketers don’t understand discounting and so the authors threw away a central plank of customer lifetime value analysis. I would argue that discounting is critical to having CLV taken seriously. If we don’t discount we can’t say the resulting number is the value of the customer so what is the number that they are calculating?

Customer Accounting, Thanks But What To Do With Acquisition Costs

The authors very firmly tell us that CLV is ‘correctly labeled’ when it is net of acquisition costs. Strangely they do this without a cite but just after citing Phil Pfeifer, my Darden professor, who rejects this approach, (footnote 8 page 26). See more here. I have ranted at length about not stating CLV net of acquisition costs. (They even cite my 2017 paper with Charan Bagga, see here, but I’m sorry to say it doesn’t seem to have impacted their thinking).

Okay, you may think they just disagree with me but are polite people who don’t want to argue or tell me that I’m wrong. I guess that is okay except when you see what they do next and how they operationalize customer equity.

Customer Equity: The Problem Of Measuring It

Customer equity is seen as a construct that includes the value of current and future customers. Still, they don’t have a convincing way to project future customers. This means they decide to only measure customer equity related to only current customers. This means their measures of customer value (rightly) exclude acquisition costs. Basically, they make a big deal about acquisition costs being important to subtract from CLV only to show the core example where they don’t do this.

A Statistical Point

By this stage, I was getting frustrated with the casualness of the argument. I’m not a statistician but I was surprised when they told us that:

There is no such thing as an average customer lifetime.

Bonacchii and Perego, 2019, page 33

Surely this is wrong. I have seen a lot of average customer lifetimes written down. I think they mean that the average isn’t useful. This is a reasonable point but terms matter. Something that is not useful can still exist. Indeed, surely that is their worry. Namely that people will use the average because it exists but Bonacchi and Perego think that people shouldn’t use it.

My big picture point is that I really don’t want customer accounting to be just the same old ‘casual with the concepts’ approach that marketers often use. We really need to be clear what marketers want before accountants can help us implement it. Customer accounting makes sense as an idea. I think we can persuade accountants of the value of the idea if we are careful. As such, we must ensure that we do not give skeptical people openings to shoot the idea down. Customer Accounting, thanks but… I think we need to tidy up the ideas before we will be totally successful with accountants.

For more on CLV see here and customer equity see here.

For more on accounting for marketing see here.

Read: Massimiliano Bonacchi and Paolo Perego (2019) Customer Accounting: Creating Value With Customer Analytics, Springer