Or, You Could Do It That Way But Why Would You Do That?

Customer Lifetime Value (CLV) is a very useful metric. (Technically, prediction/estimate I guess). It is the dollar value of a customer relationship, based on the present value of the projected future cash flows from the customer relationship. That said, it has to be one of the most mis-used of all the marketing metrics. Whenever anyone says CLV I cringe in fear that what they do will be truly appalling. How To Use Customer Lifetime Value (CLV)

Serious Problems

I’d like to say this was just me being a professor and blowing up minor issues to grade down papers but much of the advice I see simply doesn’t make sense. Work written by academics as well as practicing marketers has similar problems. See my work on CLV in teaching materials with Charan Bagga — even Harvard Business School has some unhelpful, confusing, and mutually contradictory material on CLV. The extremely popular Starbucks case is widely used but, frankly, pretty unhelpful at CLV.

When it comes to searching online you will see broadly speaking two types of advice. Some bad advice, and some truly terrible advice. It is depressing to see if you care about the quality of marketing metrics. (It is quite good to read if you want to feel superior though so it isn’t all bad).

Want Some BAD CLV advice?

Just Google ‘CLV’. This came up for me: https://www.crazyegg.com/blog/customer-lifetime-value/. As of September 21, 2020 this said: “Customer lifetime value (or life-time value (LTV), is the average amount of money your customers will spend on your business over the entire life of your relationship”. We have a number of sloppy points in the text definition alone. Is ‘money’ profit? revenue? The writer’s use of language is, at best, confusing.

In my blog I have already shared my thoughts on Qualtrics’ advice, see here.

BTW many sources make the same mistakes/seem to share elements of the same bad advice. Consultants attempting to be thought leaders seem to copy each other and converge on the same bad thoughts. I have many objections to the way CLV is taught in instructional materials: https://neilbendle.com/teaching-clv-badly/. Other people have also messed CLV up: https://neilbendle.com/more-on-clv/. To be clear this section could go on for much longer but at some point I need to become constructive and say what I think should be done rather than just criticize others which is too easy to be worthwhile.

What Should We Look For When Using CLV

Firstly, the basic (good) idea of CLV is that it brings in long-term profitability. It is theoretically superior to Customer Profit as it covers multiple periods. CLV gives a metric that allows us to better understand the full value of the customer to the company long term — not just over a short period of time.

CLV can be historic or forward-looking. (It is obviously important to be clear which you are doing). By historic I mean CLV can be used to assess the value of a customer at the end of the relationship, e.g., ‘the customer was worth $150 from the start of the relationship to the end’. While CLV itself is a prediction of what they will be worth, e.g., ‘the customer will be worth $150 going forward’.

Forward-Looking Is The Most Useful

Forward-looking CLV is generally harder to estimate — it is after all a prediction. Yet, forward-looking CLV is more interesting as it is directly useful for decisions. Generally speaking, historic CLV is probably only useful to gain information to help create forward-looking CLV, e.g., customer A looks like customer B who was worth $150 so customer A is likely worth around $150. Given historic CLV isn’t that useful I advise reserving CLV for the future-focused metric (per the MASB definition). Remember when you want to describe a past relationship using ‘Historic CLV’ should do the job.

Such a forward-looking CLV involves lots of estimates/assumptions, so although it is theoretically strong be careful when looking at CLV estimates. If you see CLV estimates push for more detail about how the metric was created. How much you plan to charge a customer in five year’s time is a hard question to answer.

Digression: A Common Mistake Using CLV

Don’t simply choose high CLV customers to invest in. This ignores the fact that funds are scarce. This will bias your customer acquisition towards high-value customers at the exclusion of more numerous, but individually less valuable, customers. I will have more to say on this in future work.

What is CLV For?

As I have a clear idea what CLV is for, I am able to say that some advice is really bad. When the advice you give doesn’t do what it is supposed to do then it isn’t that useful.

My starting position is that the value of a customer (CLV) could be useful for:

- A decision about investing in a current customer, i.e. spending on retaining, serving, & cross-selling

- Decisions about ‘firing’ a current customer

- Decisions about how much to spend on acquiring a new customer

- Estimating how much a customer base is worth when valuing a company for purchase

- Recording an asset value in the financial accounts. (This is aspirational as financial accountants aren’t keen)

Let us call this IF AVA. (I apologize, I’m not great at acronyms).

Revenue Or Profit

Many use revenue and not profit as the ‘money’ being made by the firm. Think about this for a moment. If you try and work out what a customer is worth and you use revenue you will go bankrupt very quickly.

If you are willing to spend (something approaching) the amount of revenue coming in to acquire a customer you will never cover the costs of them being a customer. Revenue can be a useful metric but using revenue in CLV is shockingly bad. (Of course, there are counterexamples of strange firms with practically zero marginal cost but let’s ignore them in developing general advice). Marketers often think finance people don’t treat them with sufficient respect. If you think revenue gives what a customer is worth to your firm you might want to consider the possibility that maybe your finance colleagues are right about you.

If You Don’t Discount

A second egregious problem is lack of discounting. Here is Hubspot’s advice as of September 21, 2020:

“To calculate customer lifetime value you need to calculate average purchase value, and then multiply that number by the average purchase frequency rate to determine customer value. Then, once you calculate average customer lifespan, you can multiply that by customer value to determine customer lifetime value” Hubspot.

To be clear this advice is comically bad in any organization where customers have lifespans longer than a fruitfly. There is no real excuse for not discounting cash flows that occur over many years. Would you be fine if someone borrowed $10 now and promised to give you $10 back in 20 years even assuming you completely trusted them to do as they say. Of course not, you’d be sure that the returned $20 won’t buy as much in twenty years time as it buys now.

Not discounting means that the resulting CLV:

I Can’t be used to decide how much to invest in current customer

F Can’t be used to decide whether to fire a current customer

A Can’t be used to decide how to spend on acquiring a new customer

V Can’t be used to value customer base

A Can’t be used to assess assets for financial accounts

What exactly is a ‘non-discounted CLV’ for then? The only thing I can think of is that you need some numbers in your report to look professional and you can’t be bothered to put meaningful numbers in.

Subtracting Acquisition Costs Before Reporting CLV

This final popular way of doing CLV is a less obvious error but is a bit more in the category of ‘you could do that, but why would you?’ People subtract acquisition costs from CLV before reporting the number to give what I will call ‘net CLV’. (Proponents just would call it CLV).

“NET CLV” = CLV minus acqusition costs

Doing this involves an additional step and makes the metric a lot less useful. Net CLV limits uses of CLV while at the same time encouraging users to make mistakes, especially in respect of sunk cost bias. (I have sunk cost bias in my cartoon book, Behavioral Economics for Kids which is available here).

What Is Wrong With ‘Net CLV’?

Subtracting acquisition costs, which are irrelevant costs, going forward means ‘Net CLV’ is not useful for any decisions involving current customers – i.e. the IF & VA of IF AVA.

‘Net CLV’

I Can’t be used to decide how much to invest in current customer

F Can’t be used to decide whether to fire a current customer

V Can’t be used to value customer base

A Can’t be used to assess assets for financial accounts.

‘Net CLV’ can be used for acquisition using the rule acquire if CLV>0. (This rule is actually incorrect when funds are scarce – i.e. pretty much all the time — but I agree it is not as bad as some of the other errors I’ve highlighted on this page). What I say in response is that subtracting acquisition costs adds no value so why do it?

‘Net CLV’ can theoretically be used for acquisition but CLV can do everything that ‘Net CLV’ does. Simply comparing CLV to acquisition cost replicates what ‘Net CLV’ does. To be explicit I am not saying acquisition costs don’t matter to acquisition decisions. That would be a very silly thing to say and I am not saying it. I am saying you can take account of acquisition costs without changing your CLV calculation. The CLV I recommend is easier to create, does not encourage sunk cost bias, and can be used for so many more purposes than ‘Net CLV.’ So what exactly is the advantage of ‘Net CLV’?

Please Don’t Subtract Acquisition Costs From CLV Before Reporting It

Key advice on how to use customer lifetime value (CLV): Please do not subtract acquisition costs from CLV before reporting it. It is harder to do, encourages sunk cost bias, and makes the metric not useful for many purposes.

Given that it is very simple to compare CLV to acquisition costs, there seems no benefit to subtracting acquisition costs before reporting CLV.

Bendle and Bagga 2016

How to Calculate CLV

You can calculate ‘historic CLV’ directly from your data.

A basic formula (there are a variety of approaches) for forward-looking CLV is:

CLV($)=Margin($)∗(Retention Rate (%))/(1+Discount Rate (%)-Retention Rate(%) )

Retention is % of customers at risk of stopping being customers who stay. (Churn measures customers at risk who leave, so 1- Retention Rate). The formula above is the infinite life formula. This projects returns to infinity (which makes the math easier and the infinity assumption makes less of a difference than one might sometimes expect).

An initial margin is sometimes claimed, i.e. formula + margin. In such cases, CLV can be written as:

CLV($)=Margin($)∗(1+Discount Rate (%))/(1+Discount Rate (%)-Retention Rate(%) )

You Can Change The Strong Assumptions

There are some very strong assumptions when using the formulas above. An obvious strong assumption is that the retention rate will be stable over time. Yet, it is very reasonable to argue that retention rate could be low in initial periods and get better as the customer pool is left with only the most committed customers. As such, it is highly debatable whether this formula will apply in your industry.

Another critical challenge is that this approach is designed for industries with regular payments from customers. Think subscription services. As you get farther from this the idea of retention is harder to conceptualize. If you are selling cereal you might wonder, “have we lost the customer or have they just not bought from us this month”. Don’t panic! There are approaches that can help deal with different scenarios. See here. Basically, don’t get too excited by the assumptions. If any assumptions don’t work in your industry don’t use them.

The CLV Definition

How to use customer lifetime value (CLV) if you don’t believe that these assumptions will hold? The basic idea behind CLV remains the same. The key thing is to follow the definition.

Customer lifetime value (CLV)….. is the dollar value of a customer relationship, based on the present value of the projected future cash flows from the customer relationship.

MASB, Common Language Dictionary

In such cases just create any CLV estimates using another method than the formula. A spreadsheet, or similar technology, will allow you to change values per period. This doesn’t change what CLV is, only how you estimate it. If someone says your assumptions are wrong this doesn’t mean that the idea of CLV no longer works. The theory behind CLV is sound but of course sometimes (often) people get the numbers wrong.

Communications Matter

In some financial valuation models CLV can sometimes be applied to future prospects to help estimate the value of the firm. This is great but there is absolutely no need to change the CLV formula to do this. Estimate cash flows from future customers easily using your preferred CLV formula/spreadsheet. Estimate acquisition costs for the same future customers. Together these inputs allow you to calculate the value of customer growth.

When acquisition costs are netted off before reporting CLV the resultant number cannot be used for decisions about current customers. This gets you to the bizarre situation where your estimates of CLV do not apply to (current) customers, only to current non-customers, i.e. potential future customers/prospects. Such linguistic contortions seem odd to me and seem likely to hamper the usage of Customer Lifetime Value (CLV).

How To Use Customer Lifetime Value (CLV): Don’t Call It Something Else

A solution to this I have seen is to call the value of current customers; residual lifetime value. This distinguishes the value of current customers from CLV. While this is clearly coming from a good place and works from a decision-making perspective this seems like a solution in search of a problem to me. I think it is useful to have CLV apply to (current) customers.

In addition, residual lifetime value seems like a term invented by finance people to apply to machinery etc… (Presumably because it is). It is vaguely demeaning of current customers as it seems to imply the current customers are a bit ‘used up’. I see one objective when advocating for more use of CLV being to improve the way we look at the importance of customers to the firm. Current customers being seen as shop-soiled seems to work against this objective. Why do this?

Digression the Common Language Dictionary

Use the Marketing Common Language Dictionary to look up the meaning of marketing terms.

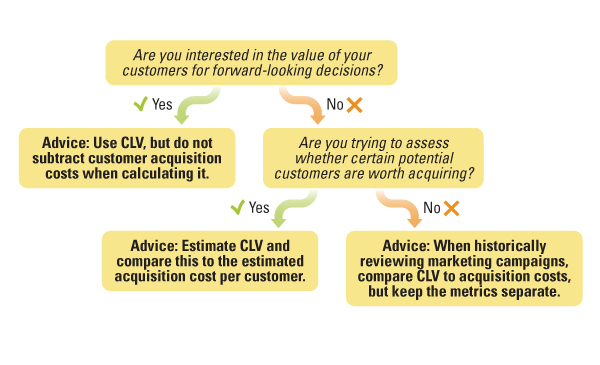

Here Is A Handy Flow Chart For How To Use Customer Lifetime Value (CLV)

The Sloan Management Review published a handy flowchart I produced with Charan Bagga.

Summary: CLV Is Useful But Be Careful

Consultants, marketers and academics have all put out pretty awful CLV advice. When using CLV you should be aware of this. If you want the metric to be useful please consider this advice.