Marketing suffers from serious definitional problems which undermine the communication function of metrics. For example, Does Acquisition Cost Reduce CLV? I therefore recommend a step forward; lets all exclude acquisition costs from customer lifetime value (CLV) calculations.

CLV Is The Net Present Value Of A Customer Relationship

Customer lifetime value is the net present value of a customer relationship. There are strong assumptions and fiddly discounting but the idea is simple. Valuing a customer is analogous to valuing a firm. When valuing a firm you determine the net cash inflows the firm will generate, when valuing a customer you determine the net cash inflows the customer will generate.

But Make Sure You Exclude Acqusition Costs

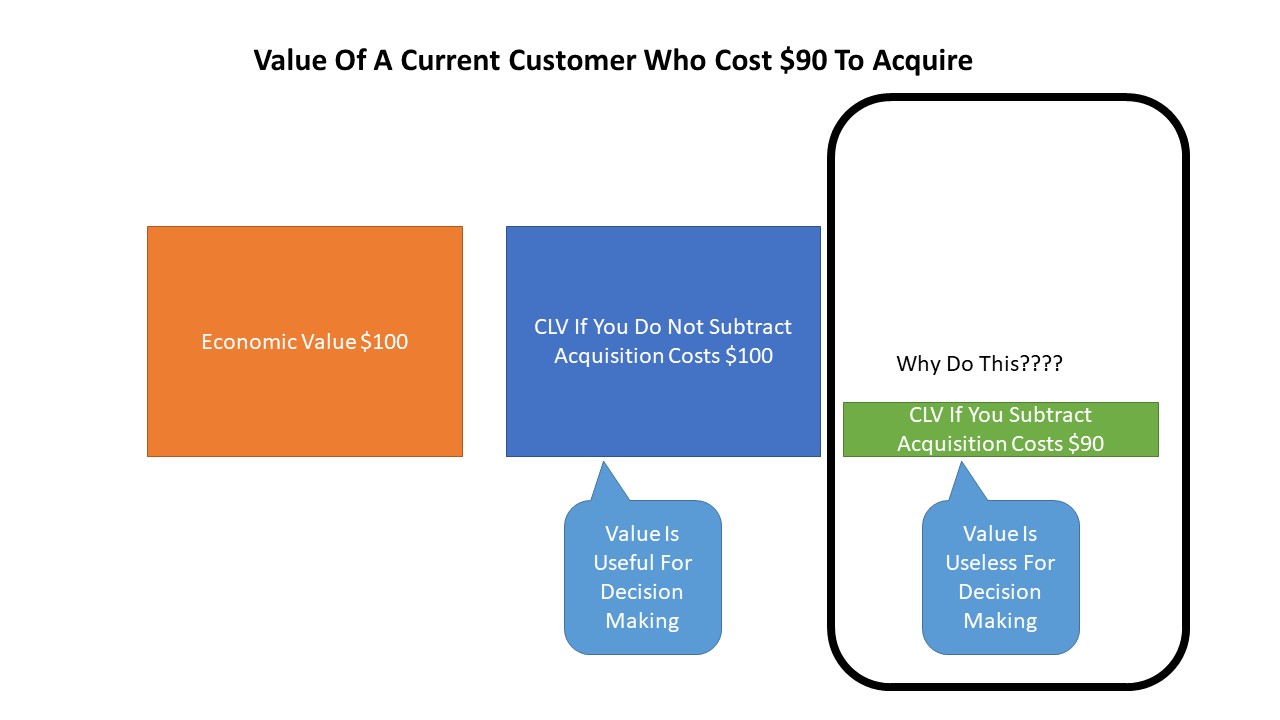

Managers naturally want to be sure to include important costs but acquisition costs should be excluded from CLV calculations. To see the problem that including acquisition costs causes imagine buying a company which has a market capitalization of $1 billion. What is the value of the company? $1 billion. You will have to spend a billion dollars to buy the company but that does not mean the company now has no value. It is worth a rather significant one billion dollars.

Similarly imagine a customer is worth one thousand dollars to a company. Whatever acquiring the customer costs the acquired customer is still worth one thousand dollars.

As some of my MBA professors noted a few years ago: “Although [acquisition cost] is certainly relevant to the prospecting decision… it is never included as a component of expected CLV.” (Pfeifer, Haskins and Conroy 2005)

Does Acquisition Cost Reduce CLV? No

Acquisition costs are very important and should be used to assess whether it makes sense to acquire a customer. That said acquisition costs should not reduce CLV or else the metric becomes a lot less useful.

For more on CLV see here.

Read: Phillip Pfeifer, Mark Haskins and Robert Conroy, “Customer Lifetime Value, Customer Profitability, and the Treatment of Acquisition Spending“, Journal of Managerial Issues, XXVII, 1, Spring 2005, Pages 11-25