Humans beings behave in ways that do not show great decision-making. Auditors are human beings. They will have bias too. How can auditors improve their behavior? How can we go about banishing bias in audit?

Bias in Audit

People’s decisions do not always correspond to the decisions of an optimizing robot. The same is true of the way we see the world. This is highly relevant to marketing. Marketers often look at the challenges consumers gain from not being a robot. There are benefits too.

Academics also look at managerial decision-making. They seek to understand what managers are doing. I personally have given less thought to the equivalent issues in audit. Auditors have to “sign off”. This means they say the decisions made by other people are correct. As such, it is extremely important that auditors make effective decisions themselves. The ACCA have a project on banishing bias in audit. (ACCA is Association of Chartered Certified Accountants). The project aims to help auditors better understand the decision-making challenges in a world where we aren’t robots.

Professional Scepticism

A key challenge in audit is being “professionally sceptical”. Clients offer the auditor information. The auditor has to determine what to accept. What to investigate further is the related question.

ACCA believes that, because professional scepticism is defined in terms of a state of mind, further improvement must be informed by an understanding of psychology.

Gambier, 2017, page 5

The idea is that a knowledge of bias can help auditors check themselves. It can also help them communicate with others.

Firstly, a standard-setting process that is informed by the literature on cognitive biases can lead to standards that either mitigate the impact of innate biases or at least avoid effects that may be detrimental to audit quality. Secondly, it may help in identifying areas where stakeholders othera than auditors may be susceptible to innate cognitive biases.

Gambier, 2017, page 5

To me this just makes sense. Any process that involves reporting to people implies that understanding how people think should be of great interest.

What Behavioural Effects Are Most Interesting?

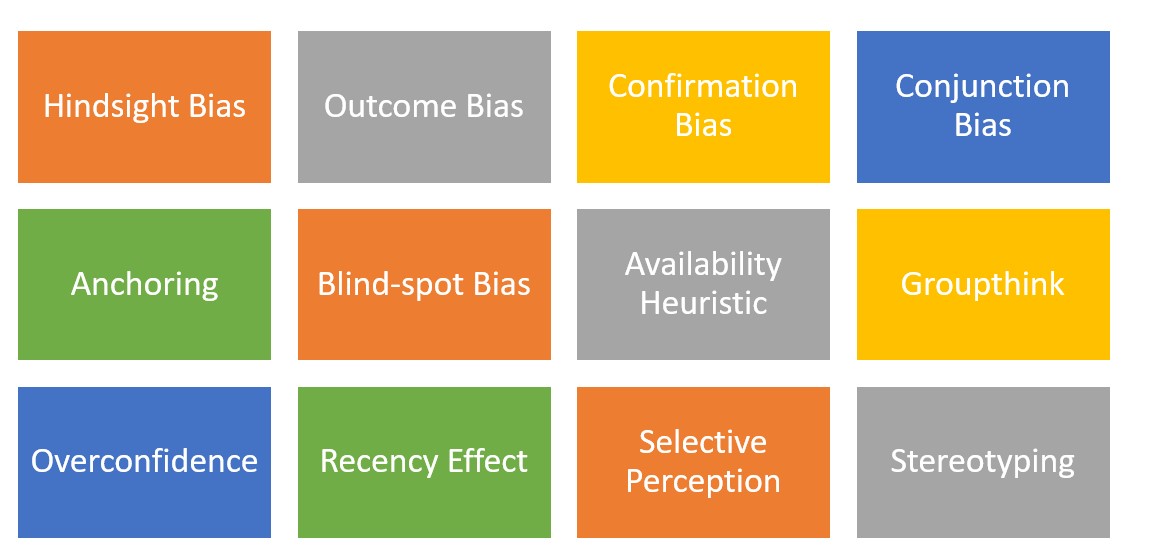

The report highlights twelve “cognitive biases”. ACCA Behavioral Biases For Auditors To Note

I’d guess confirmation bias is especially significant. This implies we tend to seek out evidence that confirms our expectations. We look for what we expect to find. And we find what we expect. This is the problem of social media and politics. We all live in echo chambers.

Looking for what they expect to find is particularly worrying for auditors. Auditors decide how much to check. They are in danger of signing off on accounts without properly investigating those items that seem reasonable at first sight. They might also not check when clients just seem honest. Looking honest really helps when you are conning people. (I imagine. I did a bit of auditing but no conning people).

******

It is fascinating to see how accountants approach these issues. I think understanding psychology is vital to effective audit. As such, it is great to see the ACCA advising its members on the challenge. Bias matters. But bias can be defeated. At least a bit. Or at least a bit if you know about it.

For more on accounting see here.

Read: Andrew Gambier (2017) Banishing Bias? Audit, objectivity and the value of professional scepticism, ACCA (Association of Chartered Certified Accountants)