Before CLV had become a big thing in marketing strategy Francis Mulhern looked at the challenge of understanding the value of customers. There are a lot of good points in the article.

Measurement Problems In Understanding The Value Of Customers

One of the most obvious challenges is that the data to allow us to understand the value of customers is far from perfect. To my mind this does, even should, change how we approach the problem. I am pretty worried about models of asset value that include the value of future customers. To my mind it is simpler to call these what they really are, non-customers. You might want them as customers but that hasn’t happened yet. For a modeling exercise/to include growth in valuations you certainly might want to estimate such values. Still, I know of no accountants who will find such numbers convincing as measures of an asset. If we are to make progress into measurement systems we might want to reserve CLV for numbers that have better data support.

Mulhern did not use the term CLV. (Preferring customer profitability, CP. I think the consensus now is to reserve the term CP for single period profitability and use CLV for multiple periods. This is a helpful distinction that has been made since the article was written). Still, Mulhern makes the important point that:

While measures of profit for both customers and prospects are important, it is much easier to build models for existing customers because detailed information on their purchases is often available in marketing databases.

Mulhern, 1999, page 28

Acquisition Costs And Understanding The Value Of Customers

The problem of good data is especially true for acquisition costs. I often note you should state CLV without subtracting any acquisition costs. I won’t repeat the sunk costs argument. Instead, I will note several other problems using past acquisition costs in decisions. By this, I mean when people use a measure of CLV after subtracting acquisition costs of a past cohort to estimate the value of a future cohort. This is implicitly done if you subtract acquisition costs from CLV and use this number to inform your planning for the future.

Firstly, acquisition costs are the first costs you incur in a relationship. They are simply more likely to be out of date than the data in historic CLV measures. Your assessments of retention costs, margins etc.. are likely to be more recent than estimates of acquisition costs for the prior cohort. Why not use more recent data on typical acquisition costs now if you have it?

Secondly, acquisition costs are usually applied to large groups only a small number of whom are acquired. Thus, you need to apportion the costs in some complex manner creating all sorts of data quality issues. You run into problems with one prospect’s decisions potentially changing the CLV of a completely unconnected customer and concerns about the nature of marginal costs in respect of a single future customer. What is more acquisition costs are likely to be less reliable than other data. Why mess up your CLV calculation with this dodgy data when you don’t have to?

Understanding The Value Of Customers: Distribution Measures

One of the things I appreciated in this paper was the attempt to introduce new measures of the distribution of customer values. The author considered traditional measures but had to change them a bit. This is because, typically, some customers are unprofitable. This means that more than 100% of profits are generated by less than 100% of customers. You need a measure that allows for this.

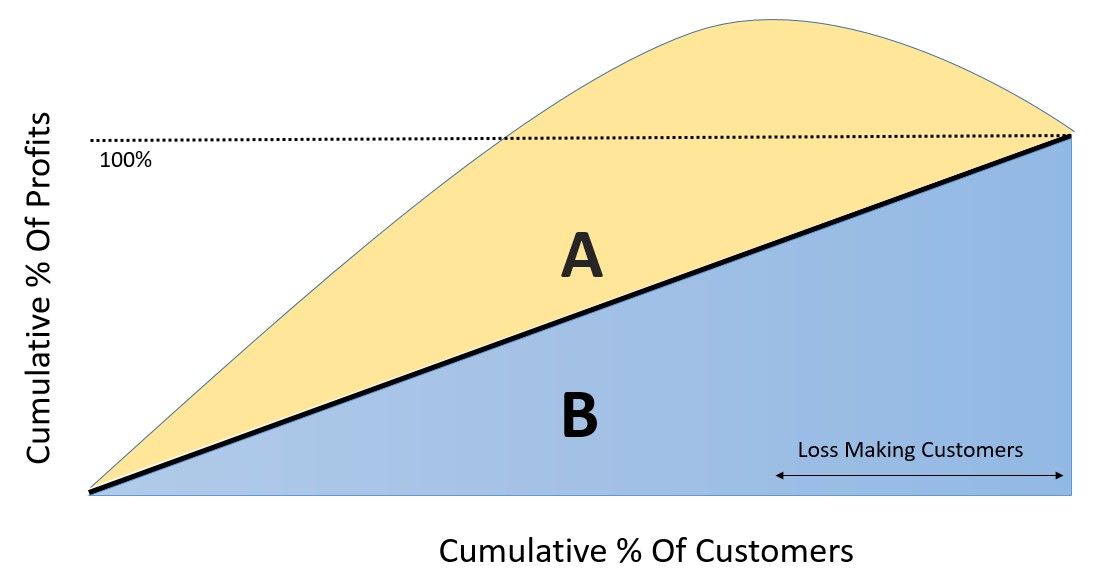

A Modified GINI

Mulhern suggests a modified GINI. Plotting customers decreasing in profitability on the horizontal axis and cumulative profits on the vertical we can create an inverted Lorenz curve (see picture). If each customer gave exactly the same profit to the firm the 45 degree line would capture the relationship between value and profits. If we were to plot every customer as completely equal then area A would not exist. Yet, A will exist as customers are pretty much never of exactly the same value. As the area, A, gets bigger in the picture we can say fewer customers are giving more of the value to the firm. (Hence why we turn to a GINI measure which typically measures inequity). The modified GINI compares the area created by non-equal profits (A) with the area that would occur with equal profits (B).

Modified GINI = A/(A+B)

where A is the area above the 45-degree line [see picture] and B is the area below the 45 degree line.

Mulhern, 1999, page 35

If all customers give the same profit A does not exist and the value is 0 (Modified GINI= 0/(0+B). Given some customers can be unprofitable A can turn out to be massive compared to B. This is most extreme where a very small number of customers give the entire value and many more customers are loss-making. Mulhern’s modified GINI can thus run from zero upwards to very high numbers.

I’m not sure that many people use Mulhern’s GINI nowadays. (Tell me if you do). Still, it is great and I really like the thinking.

For more on CLV see here.

Read: Francis J. Mulhern (1999) Customer profitability analysis: Measurement, concentration, and research directions – ScienceDirect, Journal of Interactive Marketing, 13 (1), pages 25-40