A book chapter I wrote with Jonathan Knowles and Moeen Butt has recently come out in the Review of Marketing Research (vol 18). In our chapter, we sought to give marketers a better understanding of accounting, specifically financial accounting. What then are the marketing implications of financial accounting?

Keeping Score

Marketers are trying to work out how to do well at their jobs. Yet, marketers often do not seek to understand how the score is kept. I find that really puzzling.

Financial accounting is how “score is kept” in terms of business performance. It is, therefore, in the self-interest of marketers to become familiar with financial reporting.

Bendle, Knowles, and Butt, 2021, page 15

Marketers are facing a certain set of criteria. It makes sense to investigate the criteria more than most marketers do.

Intangible Assets Break Financial Accounting

Intangible assets are those without physical form. These include such things as intellectual property, human capital, trademarks, business contracts, and customer/stakeholder relationships.

…financial accounting conventions are not well suited to a world in which intangible assets – represent some of the key economic resources of a business.

Bendle, Knowles, and Butt, 2021, page 18

This should not come as too much of a surprise. It is simply much easier to create a reliable value for something you can see and touch and more easily compare to other things that you can see and touch. A used car’s value is relatively uncontroversial. The value can be supplied to a tolerable level of accuracy. Getting a brand value is much, much harder.

What do financial accountants do when the value created by a marketing investment is hard to get? They treat marketing investments as though they are expenses — i.e. have no long-term impact. Financial accountants largely treat many (at least internally developed) intangibles as though they didn’t exist. Out of sight, out of the external financial statements.

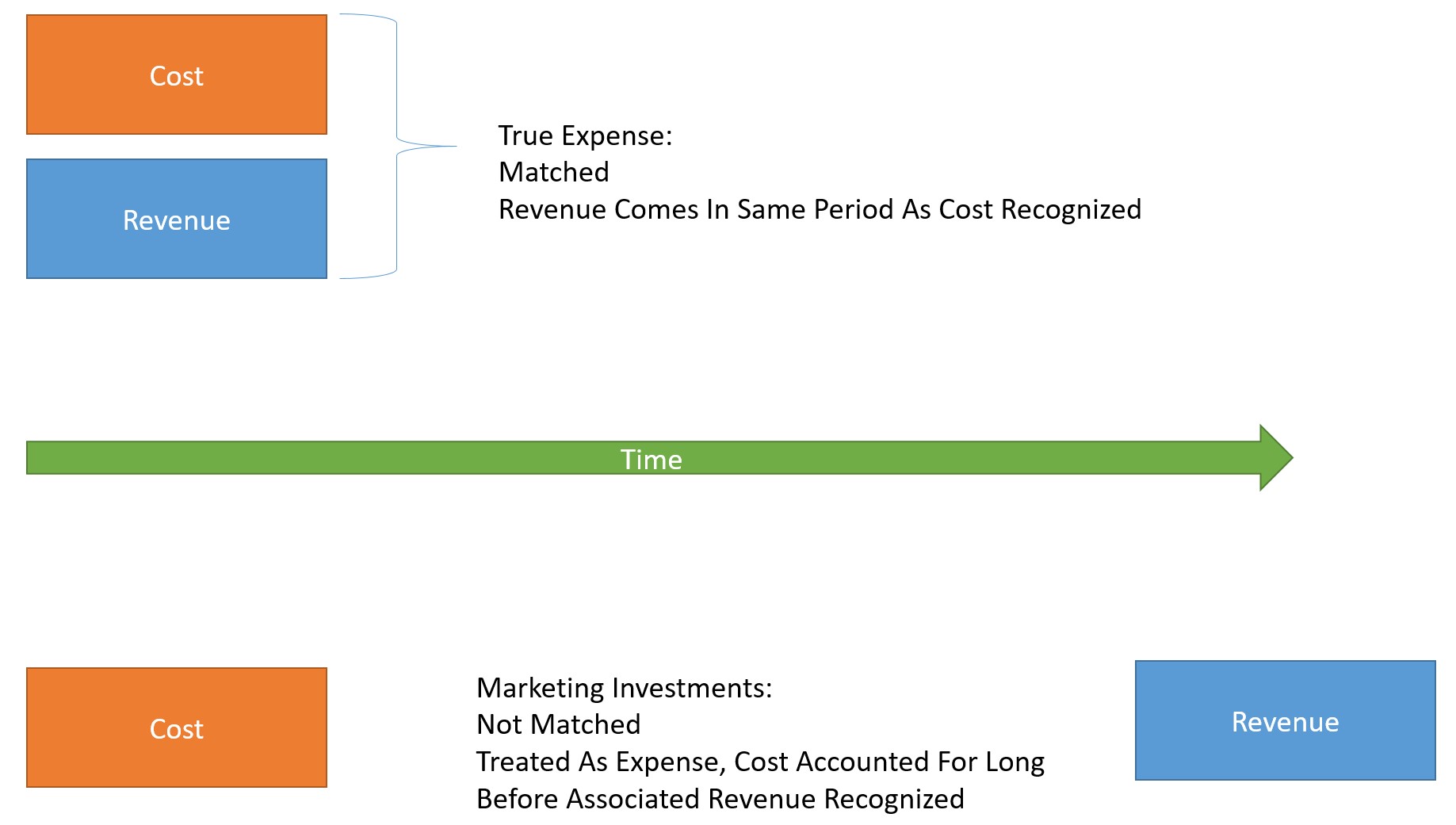

Hard To Find A Match

Life is complex. So it is worth noting that financial accountants violate their own basic concept of matching in GAAP, (generally accepted accounting principles). Matching is tying up costs and revenue. Expenses should be matched to when the income associated with them is taken. When the cash is spent should not be the determining factor

Matching costs and revenues is a major principle of financial accounting. It is the essential feature of accrual accounting, the modern form of accounting which has largely supplanted cash accounting….. Despite the obvious value of accrual accounting, the idea of matching is largely abandoned by GAAP when deciding whether to capitalize certain elements of spending (relating not just to marketing but also to employee training and investments in R&D).

Bendle, Knowles, and Butt, 2021, page 23

Think of brand-building advertising. Such advertising creates benefits that are felt in the long-term but the cash is spent now. What to do? GAAP abandons matching and goes with when the cash was spent. Does it make sense? Not really. But it ‘sort of works’ and that is just about good enough for financial accounting standards setters.

Should You Expect Any Change?

Marketers are often correct in complaining about the mistreatment of marketing investments. The treatment is usually pretty appalling. The point to bear in mind is that accountants, collectively at least, are aware that they are not supplying the value of a company.

In our experience, it comes as a surprise to nonfinancial business people that the numbers given in the financial accounts, known as book value …. do not represent the economic worth of a firm.

Bendle, Knowles, and Butt, 2021, page 18

(Good) financial accountants have no illusion that book value is the economic value of the firm. As such, marketers saying that they are missing things of value are unlikely to provoke much in the way of change. Everyone already knows this.

Financial accountants have a range of interests they could balance. Top of those currently is the perceived needs of those supplying capital. Basically, shareholders and debtors. For good or ill, this means financial accountants have decided that doing a bad job reporting on marketing is a price worth paying to avoid the risk of tricking those supplying capital. Financial accounting standards setters would rather treat a brand as worth nothing than risk stating a value that was too high.

Looking For Allies

Human Resources managers face similar problems. Investments in employees are also generally treated as expenses. How can marketers and HR work together? Sadly, I still don’t see that alliance being strong enough to motivate change. Maybe the R&D people will join in. At least the R&D people will bring cool toys. And the HR people have the best gossip.

A Note For Academics

We suggest that academics can adjust financial statements if they want. Our advice is quite rough and ready. Nothing comes for free either. Each change brings its own problems.

Of course, any adjustments made by academics inject a potentially new problem, namely that the reported results are more influenced by the adjustments made than the underlying performance.

Bendle, Knowles, and Butt, 2021, page 42

Still, the point is that a greater understanding of what the statements are will allow marketers to have a better-informed view of what is going on with the firm. I worried when we discussed Tobin’s Q that there was a lack of knowledge of financial accounting in marketing. This led to some obviously false claims that we sought to address. I am not the first to say it, but it is important to understand the bias introduced to many financial metrics and ratios from the choices made in financial accounting.

The Negative Marketing Implications Of Financial Accounting

The misrepresentation of marketing in the financial accounts has two forms of negative impact.

External financial statements are not especially useful at assessing the value that marketing generates or supplying a true portrait of the company’s economic resources. Internally, marketers cannot point to valuable assets that they are creating, nor be held accountable for errors in managing non-recorded assets.

Bendle, Knowles, and Butt, 2021, page 46

There may be reasons for many of the choices financial accountants make but marketers can still push for change. I’d recommend it. Just make sure you have a clear ‘ask’ in the language accountants understand if you are hoping for progress.

Details of the Marketing Accountability Standards Board can be found here.

For more on accounting for marketing see here. Interested in the idea of marketing accounts? See here. For more on Tobin’s q see here, here, and here. Total q is a little better but has its own issues. See here, here, and here.

Read: Neil T. Bendle, Jonathan Knowles, and Moeen Naseer Butt (2021) The Marketing Implications Of Financial Accounting, In Review Of Marketing Research, Volume 18, Marketing Accountability for Marketing and Non-marketing Outcomes