Total q is a new variant on Tobin’s q. Possibly my best-known academic paper is a piece with Moeen Butt that was published in Marketing Science. This paper criticized the use of Tobin’s q as a performance metric in marketing. I am not the only person who has concerns about the use of Tobin’s q in marketing.

As such I get the impression it is finally becoming harder to publish a paper with an Accounting Based Approximations of Tobin’s q as your performance measure. At least this seems true in better quality journals, and certainly if I am a reviewer. (For more on Tobin’s q see here and the Tobin’s q entry in my popular marketing metrics series, see here).

Now we see the emergence of a Tobin’s q variant — Total q. Some scholars seem to want Total q to have all the same magical properties. It reminds me a little of the end of the world cults. It didn’t work last time but this time its different.

Old Wine In New Bottles With A Mysterious Extra Ingredient

Spoiler on Total q — yes it is a little different from the traditional Tobin’s q. Total q is likely a little better but it is by an unknown, and probably small, amount. What is more, it gives the researcher greater discretion to massage the results. Total q still isn’t a good performance metric and I am yet to see an argument to that effect. Proponents of Total q simply don’t credibly outline how they have solved the problems of Tobin’s q in a marketing context.

Total Q: New Metric, Old Problems

While a step in the right direction Total q hasn’t got there. Indeed, it probably hasn’t even properly started the journey. It is still in its pajamas in its bedroom. The basic problem of Tobin’s q is that lots of relevant (largely intangible) assets are omitted from the denominator. This biases the metric in a direction to make intangible heavy firms look good. Total q adds a bit more into the denominator, and so seems to lessen the bias a little, but is it enough?

The simple answer is no; not if you are a marketer. This hasn’t stopped marketers lurching towards Total q. Imagine you are cheating on your spouse every night, you get caught and promise to only do it at the weekends. It might seem like progress to some but I’m not sure it solves the fundamental problem.

Total Q Adjusts For Unrecored Intangibles Which Is A Great Idea

To be clear the idea of adjusting for intangible assets is a good one. Total q tries to add in more intangible assets. I am all for this. The logic behind adding in more intangible assets to address the problem of omitted intangible assets is impossible to argue with. I would never argue with the idea that if we correct all the problems with Tobin’s q then we don’t have any more problems. That many issues with Tobin’s q could be dealt with by perfectly adjusting for omitted intangibles is correct. That said, the current idea, in a marketing context, is little more than a hope that we can fly if we believe in it enough. To be clear I don’t expect perfection but I do expect a serious attempt to at least recognize the problems.

The Devil Is In The Unrecorded Intangible Details

The challenge is that many intangible assets are not recorded. This isn’t a trivial problem for marketers or one you can just skate over. It is arguably the fundamental problem of secondary data based empirical marketing analysis. Imagine a world where you don’t have proper records of intangible assets. This makes adding them into the metric fiendishly difficult. This is the world we all live in.

Adjusting For R&D

Total q tries to find some sort of estimate of what is being omitted. How to do this? (See more here). Some R&D spending that might reasonably be called an investment is recorded but not capitalized. Financial accounting records often keep R&D under a separate line item but do not create an asset based upon it. Total q takes the eminently logical step of taking this recorded spend and doing the extra step of creating an intangible asset. So far, so good. Is the amount recorded but not capitalized an unbiased approximation of spend on intangible assets. You have guessed it, no, it simply isn’t close.

Adjusting For Everything Else

Another adjustment is to take a proportion of selling, general and administrative expense and treat this as an investment. What percentage? 30% seems to be the number. Why? Don’t ask awkward questions.

Adding an across-the-board number is crude but maybe the only practical way. Still, we know some firms invest more in advertising than others. An across-the-board number clearly adds new bias. Who knows how much? No one.

This gives you an estimate of spending on investments. You want the result of investments to understand a firm’s unrecorded assets. So you really need to estimate the value of the assets created, not the spending done. This problem is ignored in Total q. Then you need to reduce the value of investments that are decaying (amortize/depreciate). Another finger in the wind.

Corrections

The trick is that there is no good answer to the question of what is spent on marketing, see here. This is before worrying about the question of what the investments create in terms of assets. (Indeed, this is often what the analysis is hoping to estimate). Total q doesn’t answer this fundamental challenge. It just wishes away the problems with — “we correct for unrecorded intangible assets”.

To be clear I can see the value of trying to correct for unrecorded marketing intangible assets. It should be obvious we need to a) explain exactly what was done in great detail, and b) be careful when using the numbers we adjusted ourselves as our performance measures. (If you can create your own dependent variable you can somewhat pick the results you want. This should make the results reported in our papers even more impressive but not necessarily more credible).

Justification And Explanation Is Key

While we certainly wanted to argue against the use of Tobin’s q in marketing our point was actually much broader. The challenge we saw was not so much the use of Tobin’s q, but the poorly justified use of any metric. Typical justifications for the use of Tobin’s q were basically cut and pasted from what another scholar had said. Many explanations for the use of a metric seemed close to plagiarism. Quoting someone else isn’t a theoretical argument; it is a cult.

To be fair, rather than just repeating prior scholars sometimes additional flourishes were added. In a bizarre game of academic telephone, the claims became bolder and bolder. By the time we wrote out paper, the justifications for the use of Tobin’s q seemed to have become that the metric was close to pseudo-magical. It cured demonic possession as well as perfectly captured firm performance. (I am exaggerating a little, but less than one would hope). I want to try and stop Total q before we go that far.

It Isn’t The Metric It Is What You Do With It, And Where

Supporters of Tobin’s q argued that it was used in finance and economics. This was supposed to stop the reader from thinking more deeply. We, correctly, think that finance and economics both have high standards. One is expected to conclude that if it is used there it is okay for us in marketing strategy/marketing-finance. What often wasn’t explained was that the metric used elsewhere might actually be a different metric with the same name. Or the metric might be used as but one of a battery of metrics — rather than the single performance metric. Perhaps most critically what the metric was supposed to do often differed in the other disciplines.

Tobin’s q in marketing was used mostly as a performance metric, i.e., what the firm hoped to optimize. Often in finance, the metric was used as a control. Something to remove an alternative explanation. The attention you pay to a control is simply less than the attention you (should) pay to the thing that is most important to you.

Furthermore, in finance Total q (like Tobin’s q) has been proposed as a better proxy for investment opportunities, see here. Investment opportunities have a connection to firm performance but they are not firm performance to my mind. Indeed, I haven’t seen any cogent arguments to that effect. Marketers shouldn’t just import metrics without explaining how they fit with the discussion at hand. I know of no manager who ever said, “we want to maximize our investment opportunities” as an end goal.

“I Want to Believe”

The core problem of Total q remains that academics want to believe in it. It doesn’t matter that the adjustments required to make Total q work are unknown and largely unknowable. Furthermore, the necessary adjustments are likely to be smaller in magnitude when viewed from a finance perspective. Marketers generally have a wider, I think more correct, view of what is an investment than many other disciplines. (At the risk of seeming cynical I sometimes worry that any lack of full adjustment that maintains some bias to show marketing in a positive light might be tacitly welcomed by some).

Still, I am not sure that any manager has ever used Tobin’s q as a performance metric, see here. Have any ever used Total q? Unlikely. To be fair, given it is newish, will they start using Total q might be a better question? I still think it unlikely. Would managers know what you are talking about if you suggested it as a performance metric? I doubt it would make sense to any manager.

Total q is not quite as easy to compute as Tobin’s q but it remains pretty easy to use. You get some secondary data, you do some math, and, hey presto, you have some results. Ideally, you have thought of some theory before this but that sometimes seems to be an optional extra in papers I read.

Who benefits from academics finding relationships between activity and Total q? No manager or other external stakeholder as far as I can see. The only person who benefits seems to be an academic seeking to publish. Do we really need another new (to be more accurate another recycled) metric to benefit academics in generating advice that other people, rightly, do not take seriously?

Advice On Using Total Q

Don’t.

At least don’t use it as a performance metric. If you want to measure investment opportunities have a very careful read of the economics/finance literature.

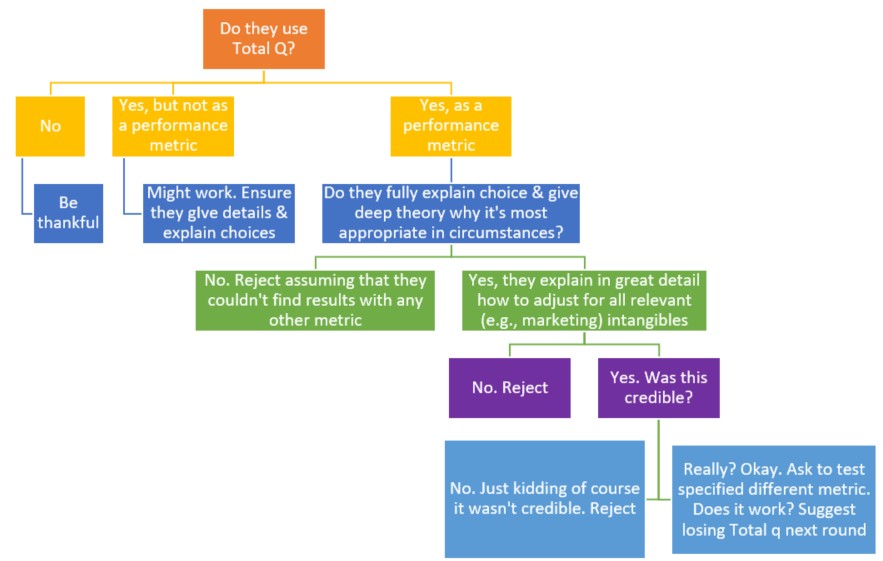

If you find yourself reviewing a paper apply this handy checklist.