I was disappointed to read Du and Osmonbekov‘s 2020 paper in the International Journal of Research in Marketing, see here. The authors clearly don’t mind hard work and I’m sure they have useful empirical skills. Still they aren’t young researchers making errors or rushing a paper to the market. They can do better. It is a Total Q mystery to me how this got through the review process.

We all make errors but the thing that annoys me is that many of their errors directly relate to those we called out in our 2018 paper on Tobin’s Q, see here and here. They cite our paper a few times which shows they clearly know about it. If they read our paper it made little impression on them. Our work didn’t stop them from merrily ploughing on spouting what I can only describe as obvious, provable errors.

Tobin’s Q Contains Intangible Assets In Its Denominator

In the economics/finance literature there is a casualness about whether Tobin’s Q has intangible assets as part of its denominator. While I am not a fan of the conceptual confusion I’ll leave economists and finance people to worry about that. To be fair there are different versions of Tobin’s Q out there. So some might not include any intangible assets in their denominator. I have seen a number of Tobin’s Q measures outlined in detail. These have all included some intangibles in their denominator. Still, it is possible in theory that there could be a Tobin’s Q measure used that doesn’t.

The good news is that when we get down to specifics we can say with certainty what happens. When Du and Osmonbekov point to Tobin’s Q they cite three papers. McAllister, Srinivasan, Jindal, and Cannella (2016) this uses total assets in the denominator (page 214) which includes intangibles. Sridhar, Germann, Kang and Grewal (2016) use total assets (page 44) ditto. Minton, Stulz, and Taboada (2019) use the book value of assets (i.e. all assets). As such, Du and Osmonkekov are simply, and clearly if you have read the prior literature, wrong to say that Tobin’s Q, as they refer to it, does not include intangible assets. This isn’t a controversial point. It is basic accountancy. It is easily verifiable by even the most a casual glance at most balance sheets.

Did They Really Read Our Paper?

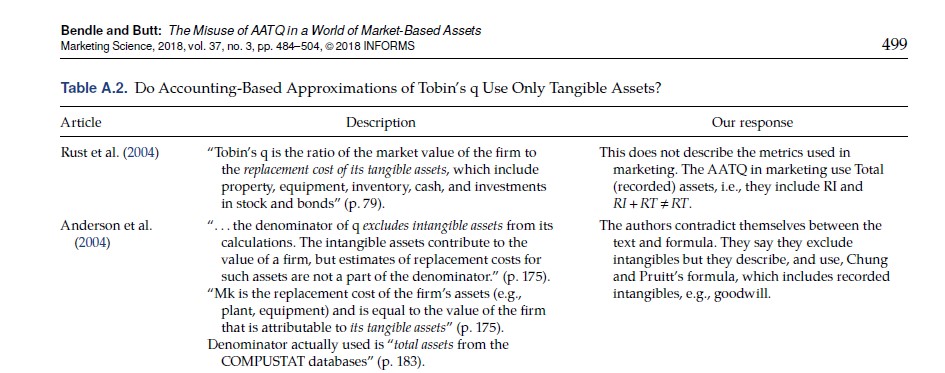

But how could Du and Osmonbekov be expected to know this? Well, they are supposed to have read our paper and we point this out in great detail. So many people previously made this basic mistake that we wrote a large section about it on page 488. This was helpfully entitled “Do Accounting-Based Approximations of Tobin’s q Use Only Tangible Assets?”. We clearly answer no, check it out here. For good measure look at table A.2 where we lay out other erroneous statements about intangibles not being included in Tobin’s q.

We also point out why they are wrong using data. Note that we say “In our S&P data, we found 24% of total assets recorded were intangibles” (page 488). How could they have read our paper and missed all these bits? It isn’t a technical discussion that we might not have explained properly. We state facts in plain English and they, after citing us several times in their paper, continue to make the same basic errors.

Is This Just a Typo Or A Total Q Mystery?

No, it does not seem to be a typo. The authors seem to believe that Tobin’s Q excludes intangibles. For example, they say:

“Theoretically, Tobin’s q excludes intangible assets of firms that account for 30 to 40% of total assets (Peters and Taylor, 2017)”

Du and Osmonbekov (2020) page 197

Yet they never take issue with our statement to the contrary. If we are wrong tell us why. Don’t just pretend it didn’t happen.

Their statement leads me to see two possbilities.

- Firstly, that their Tobin’s Q measure actually includes intangibles, they just don’t know it. This does not give a lot of confidence in their work.

- Secondly, the papers they cite regarding Tobin’s Q use a different metric to the one they compute. You will not be surprised to know that we point out this error in our 2018 paper. See also page 488 where we explictly warn against this error.

Obviously by this point we don’t really know what the authors have done. We don’t have a clear idea of their formula. To form Total Q they will attempt to adjust Tobin’s Q for unrecorded intangibles. Yet we, and probably they, don’t know whether there are intangibles already in their base number. Clearly what is in there already makes a difference to how you would do the adjustment. We don’t have confidence that they know what is in there so how can we be confident they have done any adjustment correctly?

What Is Tobin’s Q Used For?

The authors claim that “In the marketing and finance literatures [the three cites above] firm value is typically measured by Tobin’s q” (page 200). Tobin’s Q certainly was used for firm value in marketing. I believe Tobin’s Q may have been popular because it was biased towards giving results that were publishable not because it was ever a good measure. The cites they provide are all prior to our work in 2018. I would hope their statement is no longer true as the main purpose of our paper was to put a stop to this. I cannot prove that marketers have got the message we sent but I have seen no attempt to resurrect Tobin’s Q as a firm value variable.

Du and Osmonbekov’s statement also implies Tobin’s q is widely used to measure firm value in finance. (Literatures is plural so they must mean two literatures not the single ‘marketing and finance’ literature). They provide a single finance cite. This is despite the fact that we criticized this bald assertion in our paper (page 497). We argued that finance papers do not typically use Tobin’s q as firm value metric and so we need to see more evidence to support such an assertion. Tobin’s Q is certainly used in finance but I would note that finance scholars typically use Tobin’s Q as an independent variable which is very different, see here. Usage in finance, does not mean, usage as a firm value metric.

It is fine to disagree with what we said but the authors shouldn’t just repeat what we have earlier said was nonsense without further comment. They surely must have read what we said in order to cite our work. If they believe what they say they must argue that our assertion was wrong. To be clear we weren’t wrong, they don’t dispute what we said, so they just ignored us. Why is this okay?

Things Are A Bit Too Clear, Lets Confuse Everyone More

Just in case the reader is still trying to follow what they did things get more confusing. The authors seem to imply they read Total Q directly from WRDS data (page 199) which is a strange and confusing comment. They then tell us in a footnote how Peters and Taylor (2017) calculated Total Q (page 200). (For my comments on the Peters and Taylor paper see here.) They never tell us clearly what they did.

Total Q should never be used as a performance metric in marketing. Still, that isn’t even my most basic problem here. It is impossible to know what the authors did. The authors make big choices with potential to change the results that they don’t tell us much about.

Big Choices

How did they capitalize and amortize R&D? This isn’t a trivial problem. I still don’t know exactly what they did. Without this how can we hope to replicate their work?

Did they use 30% of SG&A as a proxy for investment in unrecorded intangibles? That is what Peters and Taylor did but these finance scholars did robustness checks which they could do because Total Q wasn’t their dependent variable.

I want to know is there something magical about 30%? Clearly any across the board figure used would have its own biases but the authors should at least clarify what they did so the reader can meaningfully judge any problems.

How did they use Total Q and why do they think their choices were correct in this instance? It is a Total Q mystery.

Round And Round In Circles

Here is a direct quote from Du and Osmobekov. ‘The book value of firm i’s intangibles is calculated as the sum of the firm’s externally purchased and internally created intangible capital” (page 200, my bold). What exactly does this mean? It seems to be a misquotation of Peters and Taylor who say. “We define the replacement cost of intangible capital, denoted Kint , to be the sum of the firm’s externally purchased and internally created intangible capital” (page 256, my bold).

Peters and Taylor choose the term replacement cost carefully to fit with Tobin’s theory. Du and Osmonbekov change this to book value, which isn’t Tobin’s theory at all. Book value by definition is what financial accountants record, see here. The complaint marketers have is that book value omits much internally created intangible capital. So the authors don’t seem to know what book value is. Or perhaps they have created their own definition of book value for some reason that is not at all clear to me. (Of course, they do not explain it).

Goodwill And Book Value

Indeed, Du and Osmonbekov several times restate a similar point. “[T]he book value of firm i’s intangible assets (e.g., goodwill)” to explain what is added to Tobin’s Q to form Total Q (pages 201, 202, 204). Yet, the example of goodwill is just plain odd. Goodwill is the classic example of a recorded intangible asset. Goodwill is by its nature already included in Total Assets. It therefore, already features in the Tobin’s Q measures used in marketing. Remember such recorded intangibles are what the authors don’t seem to think exist for some reason. (Technically Goodwill probably shouldn’t be called an asset but we don’t need to be that sophisticated in our thinking given we are in wonderland where everything, and its opposite, is also true). Do the authors understand enough basic accountancy to know what book value is?

Do they think of Goodwill as a recorded intangible? It is a Total Q mystery.

How Did They Address Our Paper?

They note we, Bendle and Butt 2018, said Tobin’s q “….has both theoretical and empirical limitations” (page 197) and “…questioned the use of Tobin’s q as a measure of firm value.” (page 200). This is probably a fair summary. It might be helpful to put on record that I was being polite in the published paper (and Moeen is nicer than me). I am happy to argue that one should not use Tobin’s Q to measure firm value in any circumstance.

They say that: “Bendle and Butt (2018) imply that even Total q may be problematic” (page 202). This is true. Instead of addressing the concerns they just add further analysis to beat the reader down.

Still the appropriate question becomes:

- If they think Total Q has value shouldn’t they defend it against the criticisms arising from Bendle and Butt (2018)? A proper response is to criticize our work back. We can take it. (I won’t bother listing them here but I have tons of bad points). Maybe we all will learn something if we engage in a debate. To be honest I’d be grateful for the chance to get another publication responding to their response.

- If they think Total Q does not have value, I can understand that they see no need to defend it. Yet if this is the case then why have they wasted pages and pages using it as their central metric?

What A Total Q Mystery Says About Marketing

I found this paper depressing. As I said I believe these authors have skills. The reviewers seem to have made them work hard to get published. The authors did a bunch of additional analysis that were probably at the reviewers’ requests. Yet clearly very basic things like properly reading past papers, accurate citations, and having just an MBA level of financial accounting are things that this paper shows no evidence of. This seems to me to be a pretty basic requirement if you are publishing in any field in marketing strategy, never mind a sub-field that uses a lot of financial accounting data.

We often talk about proving marketing’s value. To do so we need papers that are serious about engaging with the issues in the field. There may well be an okay paper underneath all this. But you need to be clear about the dependent variable used. The dependent variable is literally what you care about (in most cases). What happens in this paper is a Total Q mystery.

For more on Total Q see here.

Read: Ding Du and Talai Osmonbekov (2020) Direct effect of advertising spending on firm value: Moderating role of financial analyst coverage, International Journal of Research in Marketing, Volume 37, Issue 1, March 2020, Pages 196-212