My new book with Shane (Xin) Wang covers the use and meaning of Customer Lifetime Value (CLV). Being clear on the nature of the customer asset allows us to understand CLV.

What Value Are We Looking At?

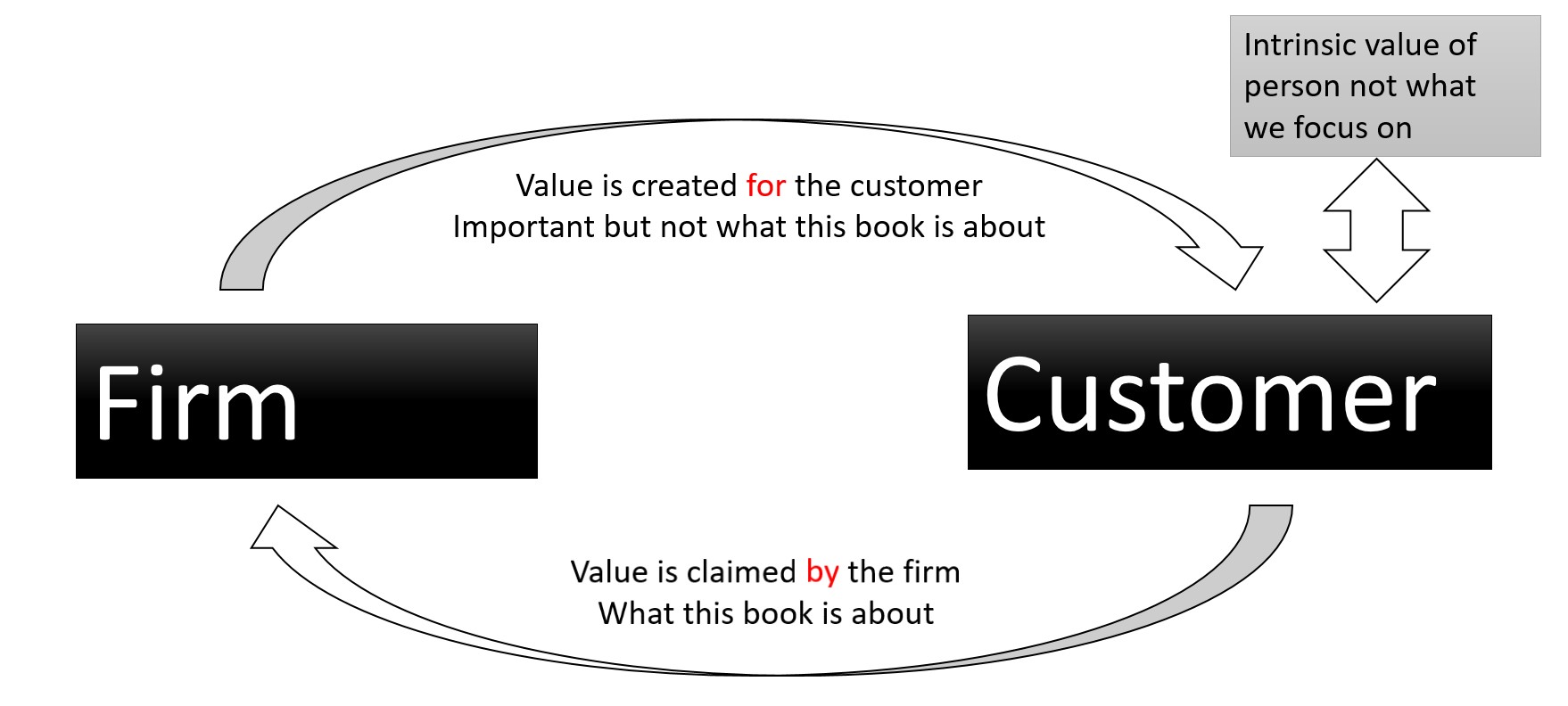

The book starts with the basics. For example, what value are we looking at when we talk of the lifetime value of customers? CLV is the value to the firm, not the value to the customer. This is not because value to the customer is unimportant. Indeed, creating value for a customer is the recommended way to ensure they continue to buy from you. Still, our book focuses on the value to the firm.

The Customer Asset

The customer is seen as an asset but this is an economic view of asset. An asset, in such thinking, is a store of value. It is not what GAAP (US accounting rules) classifies as an asset. The point is that our book looks at the characteristics of an asset and what that implies for how we should create an estimate of the value of the customer asset. This has clear implications for CLV. Given customers are an asset, and if the collective value of customers is the sum of CLVs, then CLV itself must be the value of an asset. Thus, CLV must be forward-looking. It also must not contain any sunk costs, e.g., it cannot have any acquisition cost removed from it, or else it isn’t a forward-looking value.

Multiple Uses Of The Customer Asset

A central contention in the book is that the customer asset will be more valuable — and more likely to be widely adopted — if it both has multiple uses and also fits with current accounting practice. Given accountants keep records in organizations, if a marketing value doesn’t fit with the values accounting captures these values are much less likely to be recorded. If values aren’t recorded then they likely won’t influence anyone.

We identify multiple uses of the customer assets that create the cool acronym VARIED:

- Corporate Valuation

- Customer Acquisition

- Customer Retention

- Internal Reporting

- External Reporting

- Data Flexibility

The final D, data flexibility, is a little different to the other letters in D not being a task that the asset can be applied to. (We went back and forth a bit on whether that worked — I’m still not 100% sure about our choice to be honest). That said, D for Data Flexibility helpfully illustrates the key idea that we shouldn’t have our ideas determined by data and whatever specific formulas happen to work with the particular data you might have. The customer asset is a store of value. This concept doesn’t depend upon whether you have good or bad data. Neither does it depend upon any available estimation methods for the value. The quality of numbers will differ with the data available and how you approach the data, but the basic concept of CLV shouldn’t change.

What Multiple Uses Implies

The inevitable implication of having multiple uses of CLV, and working with accounting records, is that CLV can’t seek to capture everything that might be valuable to the firm in every circumstance. There are lots of things that are entirely relevant to how good a customer is, e.g., how much they influence others through their recommendations. Many items are idiosyncratic and not captured in accounting records. These are not part of the customer asset not because they are unimportant but because for a term to have a clear meaning it must have a well-defined boundary. The point is that for CLV to be usable for many tasks it must mean something. For it to mean something, it can’t try to mean everything.

I hope you enjoy the book. If you fancy a read you can buy it here or on Amazon, here.

For more on CLV see here, here, and here.

Read: Neil Bendle and Shane Wang (2024) The Customer Asset: Understanding and Managing its Value, Palgrave MacMillan