I am not a fan of Tobin’s q (as it is currently used). I have a Marketing Science paper on the misuse of Tobin’s q in marketing. As such, I was fascinated to see a SSRN working paper with a very similar title in the field of finance/economics. The authors Robert Bartlett and Frank Partnoy, look at problems with what they call Simple q. So what is Tobin’s Q useful for? (I want to say absolutely nothing which isn’t quite true but is a decent starting point).

Tobin’s Q Became A Performance Measure (Somehow)

Bartlett and Partnoy outline the history of Tobin’s q. It morphed from being a macro-economic measure of activity in an economy to a measure of firm value. They note that: “Whereas macroeconomists rejected this simplistic version of q because of measurement error problems, law and finance scholars embraced it as a proxy of firm value” (Bartlett and Partnoy, 2018, page 1).

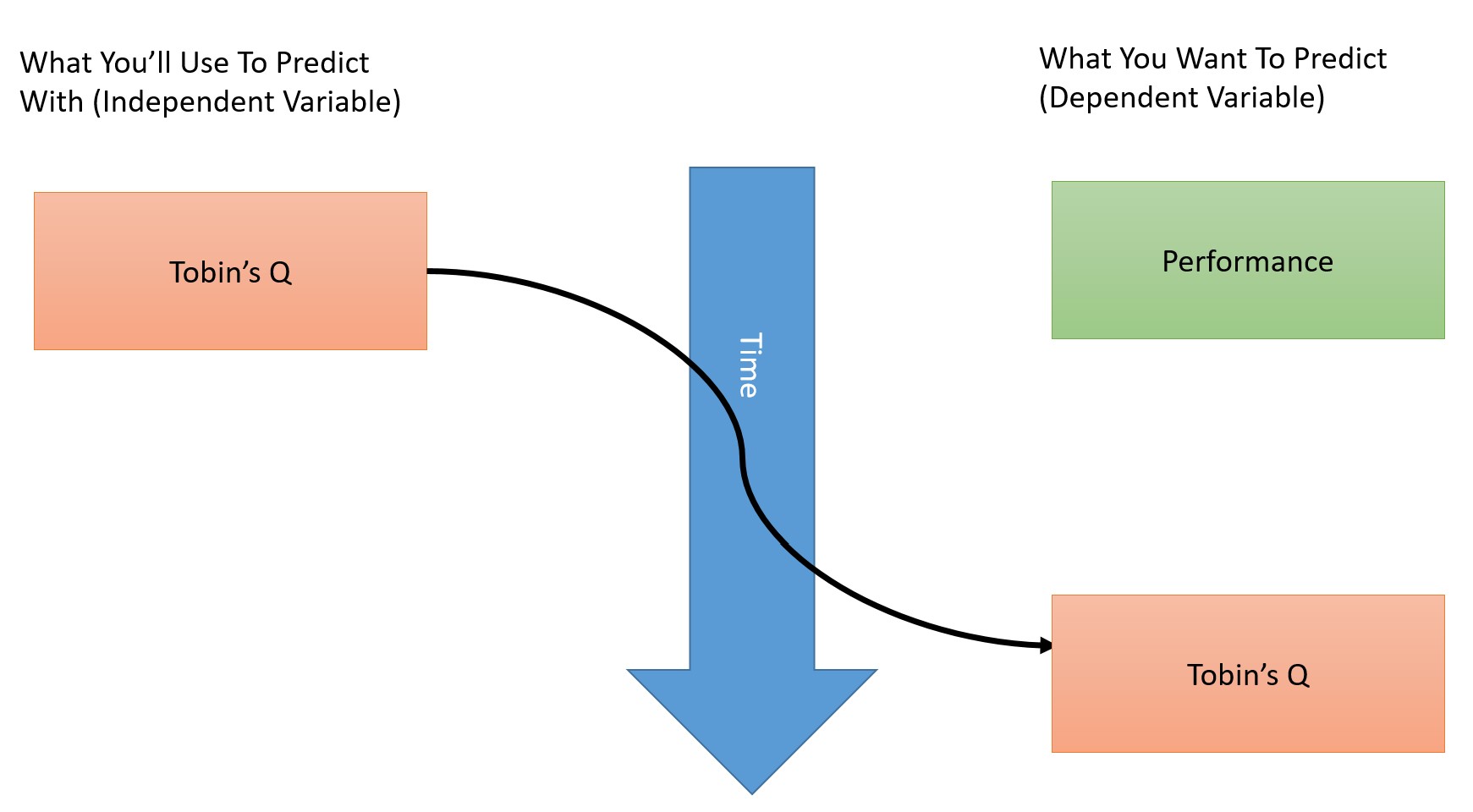

The history is interesting. The authors argue that Tobin’s q at first was used to control for market factors. In academic language, it was an independent variable. It somehow morphed to be what we wanted to predict (a dependent variable).

..Tobin’s q began its life as a potential regressor of the right side of financial equations, not as a dependent variable on the left”

Bartlett and Partnoy, 2018, page 11

Tobin’s q, for reasons that are not always 100% clear, became a presumed goal of firms according to academics. No business person I have met has ever cared about Tobin’s q. This hasn’t stopped academics claiming increasing q is a worthy goal.

Measurement Issues

The authors do a great job of outlining measurement error problems in Tobin’s q. One point they make is similar to the one that our paper focused on.

Put simply, the failure of book value to capture a firm’s investment in intangible property results in the systematic upwards bias of Simple q for firm’s that make large intangible property investments.

Bartlett and Partnoy, 2018, page 31

Note the firms with the upwards bias include marketing-heavy firms — our paper’s focus.

So what is Tobin’s q useful for. Certainly not as a measure of performance in marketing.

In Conclusion

Their conclusion is admirably clear. “Scholars should view with suspicion any assertions that firm characteristics affect firm value because they affect Simple q.” (Bartlett and Partnoy, 2018, page 50). I totally agree and it is excellent to see scholars from disparate disciples with different approaches coming to the same conclusions.

For more on Tobin’s Q see here.

For Total Q, basically the same thing in new clothes, see here.

Read: Robert Bartlett and Frank Partnoy (2018) The Misuse of Tobin’s Q: UC Berkeley Public Law Research Paper, last Revised 28 Jun 2018 Available at SSRN: https://ssrn.com/abstract=3118020