Using non-financial indicators to predict future profits.

The problem of rewarding the right things

Establishing the right reward structure is extremely challenging. O’Connell and O’Sullivan aim to help in this. They tackle the problem that traditional finance/accounting measures are quite backwards looking. (They can also be manipulated to reward those who prioritize short-term, over long-term, profits. This is because marketing and other investments are classed as expenses but that is another story). That financial metrics are mostly backward-looking is well known. It is one of the reason why “Balanced Scorecards” have become popular in the last generation. The authors discuss whether non-financial metrics, e.g., customer satisfaction, reward actions that create long-term value for the firm.

The authors make a lot of good points suggesting that introducing non-financial indicators isn’t as simple as it might be. It is challenging to find the right non-financial metrics. Some are often weak, at best, indicators of future financial performance. Also remember that almost any metric can be gamed. If you enthusiastically reward on any specific metric then managers have an incentive to maximize that metric even beyond where it makes sense for the firm. A firm could probably gain 100% customer satisfaction by giving away lots of valuable stuff but that isn’t always the best business plan. Given this, a reasonable question to ask is what metrics are most useful in any given firm?

Indicator strength

The solution that O’Connell and O’Sullivan hit upon is conceptually simple. They looked at the association between customer satisfaction and future returns on assets (ROA).

As a first step, we estimated the lead indicator strength of customer satisfaction for each individual company.

O’Connell and O’Sullivan, 2016, page 22

They used their knowledge of econometrics to try and ensure that the readings where clean ones. They stripped out things that have nothing to do with customer satisfaction.

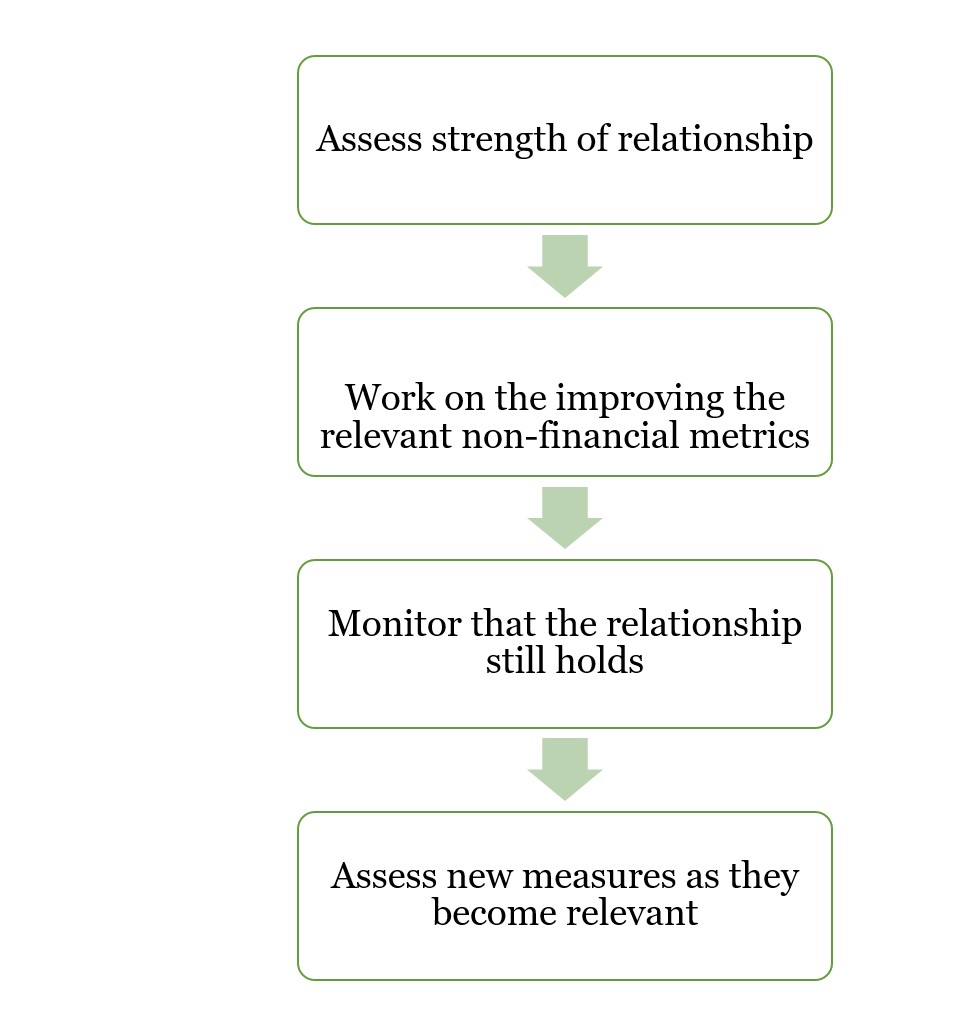

Ideally, current satisfaction is strongly associated with future returns. Indeed, it was for some firms but not for others. This left some firms that might be recommended to use customer satisfaction to reward managers but some firms that shouldn’t do it. The authors outlined their four-step process and it seems sensible.

- Assess strength of relationship

- Work on the improving the relevant non-financial metrics

- Monitor that the relationship still holds

- Assess new measures as they become relevant

My Concern: Without Theory Models Aren’t That Practical

I see is the lack of theory in their model as a problem. It all seems too driven by the data. This sounds like a good thing. Letting the data talk and all that. Yet, it means you can’t simply answer reasonable questions about the incentive system you are planning to adopt.

Why this metric and not another? The answer is that the model suggested it. This isn’t very satisfying, especially for people who can’t follow the econometrics, i.e. normal people. That said, other models, using ROI instead of ROA for the return etc…, would have suggested other metrics. It can seem a little arbitrary. Basically, because it is.

Using Non-Financial Indicators Long-Term

When do we decide that the relationship no longer holds? Do we change our entire reward system if the relationship misses one quarter? If not, how long do we wait?

Furthermore, how can managers plan their actions? Their reward system might change without them knowing why? How is this reward system motivational?

It is sensible to worry about the strength of associations in data but it isn’t enough. To be fair the authors would almost certainly agree. I don’t mean to imply that they don’t know this but they don’t have space to discuss it in their piece. This just means there is much more work to do.

For more on the balanced scorecard see here and here.

Read: Vincent O’Connell and Don O’Sullivan (2016) Are Nonfinancial Metrics Good Leading indicators of Future Financial Performance, MIT Sloan Management Review, Summer pages 21-23