Alex Edmans’ Grow The Piece is a useful book trying to refocus business on being beneficial for society. I have noted the key points on this before, see here. Here I’ll tackle a grab bag of points related to Edmans’ book and using a pie-growing mindset.

Maximizing Shareholder Value Is Nebulous

Often people like the idea of maximizing shareholder value because it is ‘simple’. You know who the shareholders are, but stakeholders are tougher to identify. Still, one challenge is that maximizing shareholder value is a bit of a nonsense phrase. It reminds me of Melania Trump’s “Be Best”. It is basically a bunch of BS to distract everyone from the lack of a meaningful philosophy. (I think Milton Friedman largely punted on the tough issues in his famous argument for shareholder primacy, see here.) In addition to the philosophical questions about what firms should do there are fatal measurement issues to the idea of maximizing shareholder value. To be clear, we don’t have meaningful ways of knowing whether we are maximizing shareholder value before we take an action nor do we know whether we maximized it looking backwards.

“’Maximize Shareholder Value’ is theoretically appealing but practically unworkable.”

Edmans (2021) page 61.

Executive Pay

Edmans gives a fairly robust defense of executive pay. I presume he didn’t want to be seen as mushy by corporate types. His points are not totally off but I didn’t think he was especially compelling. For example, he says,

“In a CEO context, fairness is pay that’s proportionate to her contribution – pay should reward value creation.”

Edmans (2021) page 177

Sure. That seems fair in many contexts not just when we are talking about CEOs. The more value you create the more you might reasonably expect to be paid.

I accept that Edmans might have an aversion to hard and fast rules. It is a fair point to argue about. Theoretically, why must CEO pay be less than an arbitrary multiple of the average worker’s pay according to law? It is true to say that it can be really hard to know what the right level of executive pay is. This does count against those who criticize CEO pay, they can’t prove the CEO isn’t worth it, but the argument is double-edged. Those who try and justify CEO pay aren’t any more effective. They find it hard to show that CEO pay isn’t excessive and looking at it leads most people to think it is.

What Is The Value Created?

The problem is that understanding how value is created is very hard. Edmans says:

In 2017, JP Morgan CEO Jamie Dion was lambasted for a ratio of 364 [of CEO pay to average worker pay] – but the stock price had risen 62% over the past two years.

Edmans, 2021, page 177

I am sure he would agree that this anecdote, while interesting, isn’t meaningful evidence. We aren’t really interested in whether the share price had risen 62% or by any other amount. We are interested in how much more it rose because of the CEO’s work that Dimon in particular did. More specifically we want to know what did Dimon bring to the role compared to the next best alternative to hiring Dimon? Anyone know this? Nope. Of course, no one knows this. So, if you want to defend Dimon great. If you want to lambast him too, then go right ahead. The evidence isn’t compelling either way.

Showing CEO Value

Empirical studies do get into this, but they are yet to be truly conclusive. (This isn’t a criticism — one can’t expect a magic study that has “the answer”). Edmans does note research that suggests CEOs at better-performing firms get paid more. This seems reasonable enough. I’m certainly for such research but I have never seen anything that can really answer the question of what CEO pay should be and I’m not sure Edmans has either. Consider a couple of problems.

Value Creation And Claiming

A) Value creation requires lots of people to do it. Even if the share price is a good proxy for the value of the firm the increase only came because of the whole team’s actions. How should the contributions of each team member be judged when the outcome is from the interaction of the efforts of all of them? Generally, the people running the firm decide who is contributing most. (People of the CEO’s own social ilk, including various golfing buddies on remuneration committees, also have a strong say on CEO pay.) Such people think it is mostly the heroic CEO who deserves the Nemean Lion’s share of the rewards. Are they right? Hard to say for sure, but I think a little cynicism is in order.

B) Remember as well that CEOs create value for other stakeholders. As such, think of CEO pay as akin to a commission. They absolutely should not claim 100% of what is generated. If that were the case, why would anyone bother to hire them? So, is 1% of what they create the right amount of commission? Is .1% or 2%? Who knows? Even if better CEOs get paid more than worse CEOs this doesn’t mean they aren’t all being paid too much. (Or I guess too little. Still, I’m not too worried. I think they can stand up for themselves).

An Efficient Market For CEOs

Here we could talk of markets setting the rate but is the CEO market efficient? Efficient markets rely on a number of conditions such as the ability for buyers and sellers to learn and the provision of useful and reliable information. It is really hard to be confident that the CEO market is efficient given so little learning about the alternatives happens. Is everyone who wants to have a go at being a CEO given the chance so we can see how they do? No, of course not. It is likely that there are people out there who could do a great job. Even those who would do a much better job than the current crop of CEOs. Sadly, they will never get the chance and we’ll never know what we are missing.

Some could just point at CEOs and argue they are all clearly brilliant people at the top of their games. Are CEOs all geniuses? Not really. I loved the story of Wells Fargo choosing ‘Going for Gr-Eight’, to aim for 8 products being sold to each customer. Why? Because it rhymed. It did not turn out well. There are plenty of CEOs who don’t seem to be geniuses. Is the market really ensuring the cream always rises to the top? Maybe a little cynicism is in order again.

Errors Of Omission And Commission

An interesting feature of Edmans’ discussion is the argument that errors of omission (what you don’t do right) can be more consequential than errors of commission (what you do wrong). People tend to have more sympathy with not doing stuff. This can be understandable given there are any number of good things that we don’t do. We can’t easily be blamed for everything we didn’t do, but we can easily be blamed for what we did do.

Trolley problems in experimental philosophy often come down to people not wanting to take a negative action even if the lack of action allows a much worse negative event to happen. (When the worst outcome happens it isn’t seen to be the inactive person’s fault. Indeed, some seem to think keeping your hands clean is more important than making the world better). I have a lot of sympathy with Edmans here. I agree with him that we often focus on doing no harm when sometimes we need to focus on actively doing good.

Actual Data Includes Survey Data

Where I banged my head on the table was when Edmans revealed his personal bias. He studies secondary data, which is collected for another purpose than the research — e.g., he studies financial accounting or government data. Anyone who has worked with secondary data knows that it has loads of challenges. There is always missing data, dodgy decisions in the compilation of the data, inappropriate operationalizations etc…. Edmans clearly sees secondary data as acceptable data despite the really obvious problems it has. I’m good with him here. Nothing is perfect after all. Use what you have got and make your conclusions somewhat tentative when the data is imperfect (as it always is).

Yet, when warning people that there are problems with claims he suggests one should check if research is based upon ‘actual data’. This seems sensible. After all, I believe him that a lot of claims don’t come from studies — they are just made up. Still, as an example of this problem, he suggests that “numerous studies aren’t based on actual data, but simply asking people their opinion” (Edmans, 2021, 385).

Why People Hate Finance Professors, And Why They Deserve It

This was deeply frustrating. Edmans is a finance professor, and he seems to have implicitly bought the nonsense spewed by many in his field. This is why no one likes finance professors, and many deserve the opprobrium. Survey data is (drum roll) actual data. It always has been, and it always will be. It shows siloed thinking to imply otherwise. Of course, Edmans is correct to say that asking people their opinions is not the same as finding data on their behaviors. Always check the data claims are based upon. One should never pretend survey data is the same as, for example, scanner or financial accounting data. Yet both secondary data and survey data are both ‘actual data’.

Pieconomics

At the risk of seeming too much like a marketing professor, when reading the book I couldn’t get over the central term for Edman’s pie-growing. He calls his ideas Pieconomics, Pie-co-nomics. This felt to me like a really ugly term compared to the other obvious option, Pie-nomics. I’m prepared to admit my feeling is only a hunch. Maybe most people prefer Pie-co-nomics to Pie-nomics and Edmans made the right choice. I have a solution. He should have surveyed people and asked their preferences. If only he believed that this was ‘actual data’.

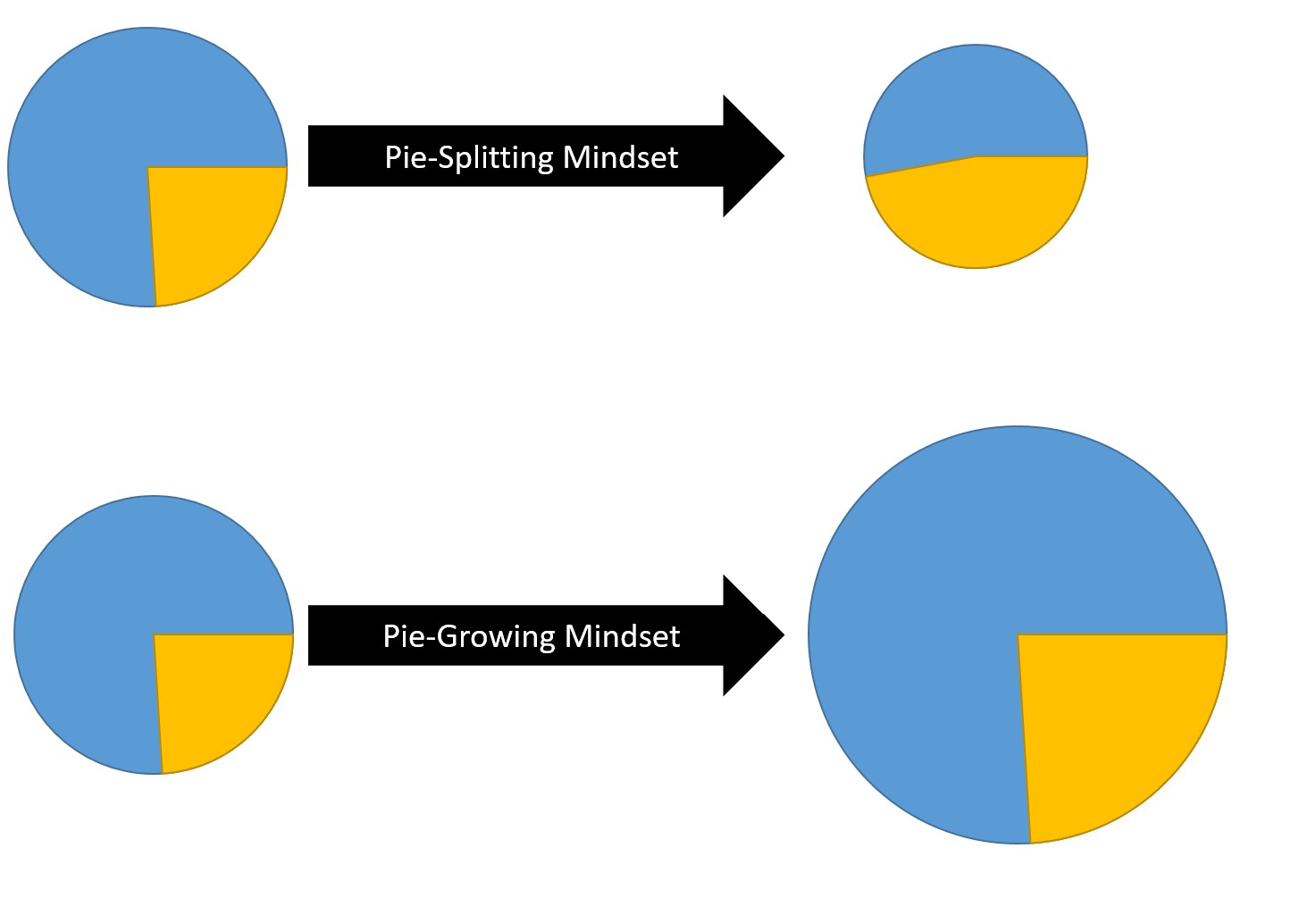

Using A Pie-Growing Mindset

Using a pie-growing mindset is great advice. Let’s do it even if we have to use survey data to do so.

For more on social dimensions in business see here, here, here and here.

Read: Alex Edmans (2021) Grow The Pie: How Great Companies Deliver Both Purpose and Profit, Cambridge University Press, https://www.growthepie.net/