An interesting topic in consumer behavior is that people experience ‘pain’ when paying for something. One can think of this as a good thing. We obviously do find joy from gaining the stuff that paying acquires. If, therefore, we didn’t feel any pain when paying we would all end up spending too much. Thus, there is considerable discussion about what drives the pain of paying. Those concerned with consumer protection generally don’t want to make it too painless to pay. If so consumers might do a lot more of it than is good for them.

Changing The Pain Of Paying

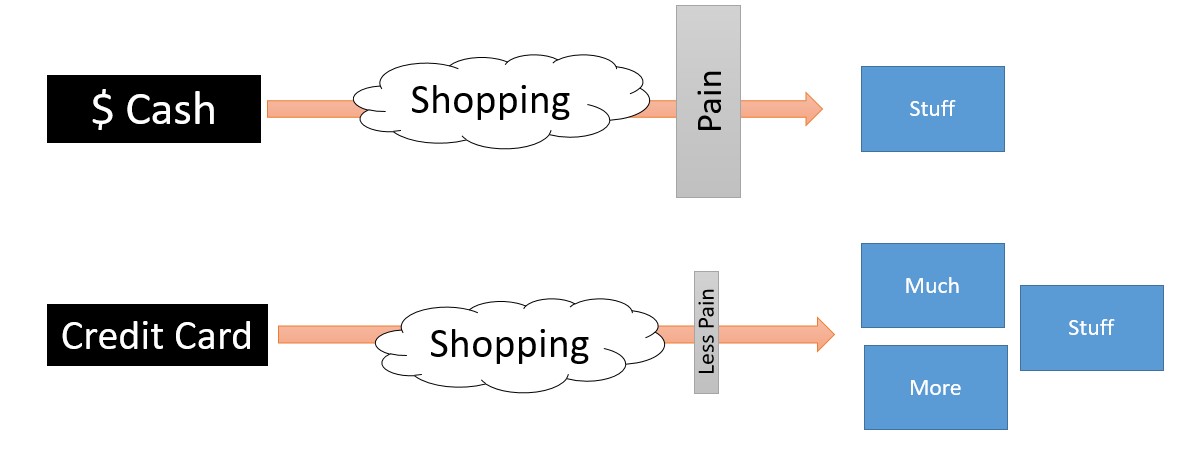

Different payment forms can change the pain of paying.

[T]he manner in which consumers paid seemed to influence how much they would pay”

Soman, 2003, page 174

Thus, scholars have looked into which payment forms can make it ‘too painless’ for consumers to spend. Perhaps unsurprisingly credit cards and other electronic forms of payment are often less painful than paying cash. As a result credit cards are often overused.

Dilip Soman (2003) argues, and supports with data, that payment transparency impacts the pain of paying.

We define payment transparency of a payment mechanism as the relative salience of the payment, both in terms of physical form and the amount, relative to paying by cash…. Cash is the most transparent form of payment – when one pays by cash, one sees exactly what they are paying….. At the opposite extreme, a completely opaque (non-transparent) form of payment might be a payroll deduction that one is not even aware of.

Soman, 2003, 175

The Value Of Imperfect Experiments

In a series of ‘imperfect’ experiments, i.e. trying to see an effect without being able to do proper random assignment, Soman saw how payment form impacted spending. For example, he collected grocery receipts and found that:

The reduction in transparency of payments [from cash through checks to credit cards] increased the dollars spent, but only on items whose consumption was flexible but not on items whose consumption rates were inflexible.

Soman, 2003, 182

Given little discretion, such as for staple foods, people bought what they needed whatever the payment form. Yet, consumers were more likely to spend on less essential goods when using a less transparent form of payment, like a credit card.

As someone who is a fan of electronic payments I think it is vital to understand (and mitigate) any negative effects. Any problem might be exacerbated by moves towards a cashless society.

For notes on public policy and behavioral economics see here.

Read: Dilip Soman (2003) The Effect of Payment Transparency on Consumption: Quasi-Experiments from the Field, Marketing Letters 14:3, 173–183