Roger Sinclair shows the value of experience when he surveys the history of reporting on brands. (Roger made a large number of contributions to the field of marketing accountability. I had the honor of presenting Roger’s family with the Blair Award for Marketing Accountability at the 2019 MASB Summit see here).

When Firm’s Reported Their Brands

Sinclair describes a time when firms would add brand values to their balance sheet. The challenge was there was no recognized method for doing this. Firms just used whatever method they fancied. That lack of agreement on the method to use meant it seemed like firms were just trying to mislead investors. This led to the issuance of “a “cease and desist” order” (Sinclair, 2016, page 168) in the UK. Other countries followed suit.

Sinclair clearly has sympathy with the ultimate goal of the firms told to cease and desist. He, correctly, notes that market value has become increasingly detached from the values in financial accounting statements. In essence, it is hard to see why anyone would pay too much attention to the financial statements. Many of the more important details about the firm’s assets aren’t entered into them.

Reporting Brands As Assets

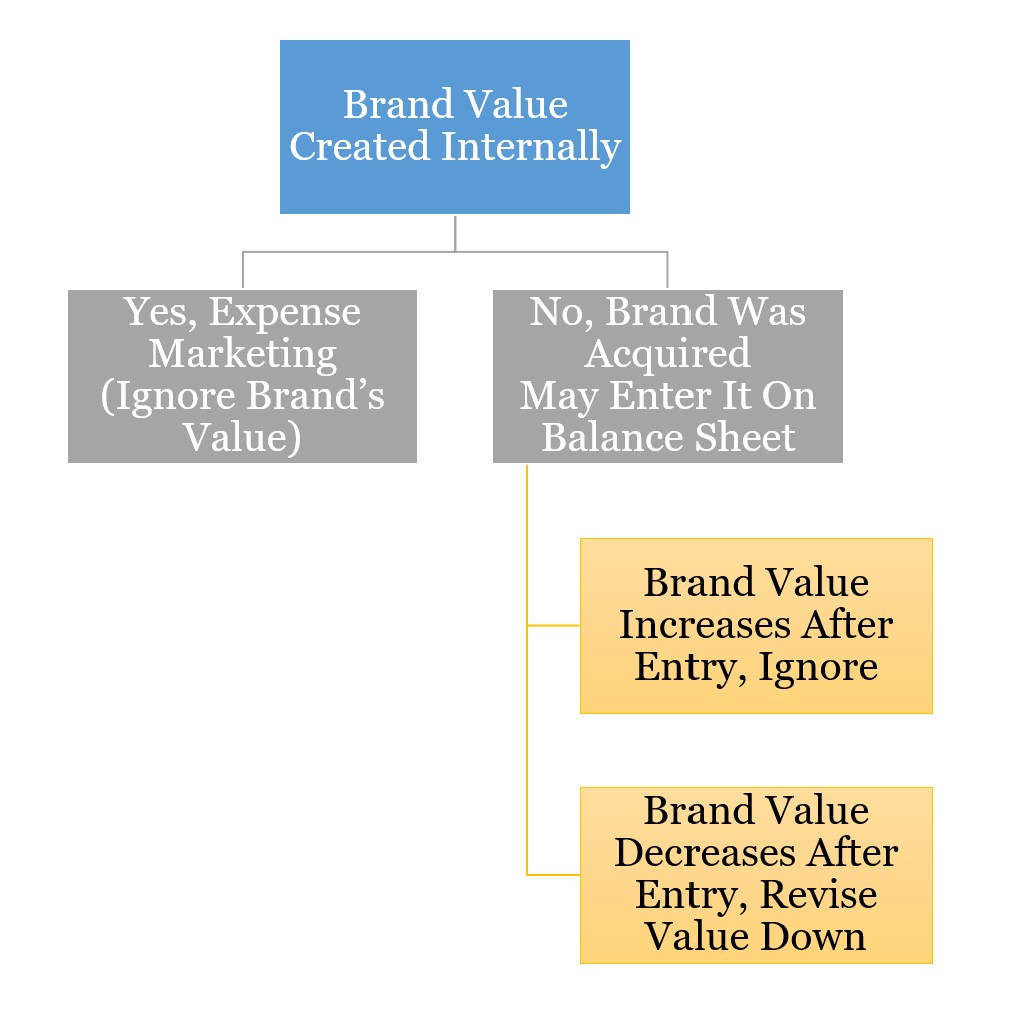

Sinclair points out the obvious problem at the moment. Although brands mostly aren’t classed as assets, sometimes they are. What is more, this classification has nothing to do with the brand’s value. The balance sheet may see a brand entry when the brand is acquired. Thus, an acquired brand is recorded. Still, a brand of exactly the same value that was internally generated is not. Accountants can see the problem with this weird double standard. (At least those I talk to can). Still, recording internally generated brand values, the concern goes, could create a worse problem.

Brand Values Only Go Down

Even when brand values are recorded they tend to only be adjusted down. If values increase they stay the same on the balance sheet. This leaves the numbers largely irrelevant. Sinclair, therefore, suggests that there is a perfectly good accounting procedure to increase the value of brands when they go up — accretion.

The term accretion is the opposite of impairment.

Sinclair, 2016, page 174

Again accountants don’t tend to like increasing values. Yet, not increasing the value of a strengthening brand does mean that the recorded brand values can become increasingly meaningless over time.

The sides are quite a way apart on balance sheet recognition. I find it a great debate to have. The history of reporting on brands suggests change is possible.

For more on financial accounting and marketing see here, here, here, and here. (And much of the rest of this website too).

Read: Roger Sinclair, 2016, Reporting on Brands, In Accountable Marketing: Linking Marketing Actions to Financial Performance, Edited by David W. Stewart and Craig T. Gugel, Routledge, MASB