Daniel McCarthy and Fernando Pereda have a paper on the role of customer equity in corporate valuation. It is on SSRN so a working paper and yet to be formally published, see here. Still, it has been downloaded a lot. So, I think it reasonable to take a look and comment as many have already seen the work. It has many excellent parts. Indeed, the key point is absolutely necessary to understand and I agree had largely been missed in the marketing literature. What they address are some great questions to discuss.

Role Of Customer Equity In Corporate Valuation: Not Maximization

The authors point out a widespread problem in the prior marketing literature. Namely the suggestion that the aim of a firm should be to maximize its customer equity. We’ll return to defining customer equity but the idea of maximizing customer equity, as the authors rightly point out, is a bit odd. Why would a firm seek to maximize one aspect of its business at the exclusion of all other considerations? Property values are important to a real-estate firm. Yet, the firm shouldn’t just buy properties willy-nilly. Critical things, like how much it costs to borrow to get the properties, also matter.

Customers are important to firms. Still if, as many do, you think shareholder value is your objective you have to think a bit more broadly than just the value of customers. (The purpose of a firm is a controversial area but the authors have a clear position so we’ll largely assess things using their perspective).

Customer Equity

The authors make the important point that customer equity is a misnomer. I mentioned this in my page on Customer Equity, see here. My explanation is a little different than theirs. Still, I read McCarthy and Pereda’s paper before writing my page so while I didn’t consciously use their idea it may have been in the back of my mind. Fair dues to them.

The authors even suggest customer asset value as a term. Something I have subscribed to as well. Though I see the customer asset as different to their version as I will note below.

Costs And Where You Look From

Accounting for costs is a bit of a nightmare. The authors make an important point that we need to consider variable costs however they are accounted for. They tell us that any variable proportion of indirect expenses must be deducted in the CLV equation. Their logic is good but the challenge with the data they use is that external parties doing the valuation don’t really know what costs are variable. External parties use estimation methods. A manager working inside the firm should, thus, have a potentially better view of customer value than the external analyst. The external analyst does their best with the bad data they have. I believe that managers are ill-advised to borrow methods from (external) corporate valuation when they theoretically can do better by looking internally.

Is Customer Equity A Valuation Or A Management Strategy Term?

A challenge with coming at customer values from corporate valuation is that it seems like the tail wagging the dog. The idea of customer equity is broad. Beyond valuation customer equity often involves the idea of managerial strategy. I even think ‘customer assets’ can help provide a unified theory in marketing strategy. To be clear, in saying that, I go farther than most scholars I know.

To see why, to my mind, external valuation can’t really determine what we decide is the customer asset we can turn to the literature. Indeed, the paper McCarthy and Pererda said got everything going, Blattberg and Deighton, 1996, I’d class as a managerial not investor-related paper. Customer valuation started for managers and the needs of corporate valuation shouldn’t determine the choices marketers make in their internal management decisions. Instead, I’d aim to develop a theoretical perspective that can be applied by managers using their better (internal) data. The corporate valuation people can then try and replicate the internal view with whatever data they can get their hands on.

What Is Customer Equity And CLV?

The authors note that customer equity is often seen as the sum of the CLVs of the firm’s customers. They correctly note that CLV definitions are all over the place. (And include an excellent table to make their point). If CLV is ill-defined this necessitates that customer equity is also ill-defined. To solve this problem they suggest a new definition of customer equity. To make this work they then need to redefine customer lifetime value. This means they end up with a new definition of both customer equity and CLV.

Change Is Good

To make this seem less radical they ‘claim’ past work as using their approach. For example, they claim papers followed their approach “even though these papers had formally stated CLV-based…definitions” (McCarthy and Pererda, 2020, page 8). I.e., the early papers used a different definition to the one they suggest. The contortions of language were all a bit too “1984” for my tastes. Don’t believe what you read; this is what the prior researchers really meant. The authors’ fundamental problem is that they want to argue they are following the past literature while also wanting to change it. To my mind, you either,

- claim the past literature is clear — in which case you can reasonably argue it should be followed. Or you,

- claim the past literature is a mess and you solve the problems — in which case you can’t reasonably claim your work is supported by the prior literature.

For the record, I think 2) — CE is a mess and needs to be changed — is the more fruitful approach.

A Problem For Retention Marketers

To be clear, the authors’ approach works in numerical terms. Indeed, the terms they used may well suit a finance/corporate valuation perspective. Still, any marketer who has ever talked about using the CLV of customers in retention decisions would be deemed wrong under their taxonomy. It feels like putting the finance cart before the marketing horse.

Is There A Role For Customer Equity?

The authors and I share the view that customer equity is problematic. Still, I felt they could have been clearer about getting rid of customer equity. They did not want to insult the prior work too much. (To be fair I understand, given peer-review you don’t get published insulting prior work). So, they suggest customer equity is a mess of a term but still try to argue that it remains a useful concept that they employ.

If customer equity isn’t equity (as they rightly note) and it isn’t defined the way people have defined it in the past it isn’t clear to me that the old view of customer equity still has a role. I’m absolutely not saying that customer lifetime valuation, customer metrics, and customer assets etc.. don’t matter. Just perspectives must change given the flaws in the prior views of customer equity that the authors correctly note. Instead, they seek to follow past research in claiming that customer equity will become the dominant marketing paradigm. This is like saying that Galileo basically followed the Ptolemaic paradigm because his ideas were all about planets and stuff like that. Apparently, peer-review is scarier than the inquisition.

What Is Customer Equity/The Customer Asset?

The authors outline a new definition of customer equity, what I’ll call the customer asset. My definition is simple; the customer asset is the sum of the CLVs of the firm’s customers. I basically just adopt the traditional definition of customer equity but use the term asset instead of equity.

To be fair many in the prior literature have, like these authors, taken a more ‘maximalist’ view of CLV than I do. In doing so the maximalists (my term) include the value of future customers and their acquisition costs in the value of customers. One reason for my ‘minimalist’ view is that I think it is hard to call future customers a customer asset when you don’t have a relationship with them. Future customers aren’t, after all, currently customers and so don’t logically seem to be part of the customer asset.

Still, the authors tell us in their paper that they will provide the “best” definition. So they clearly think they have a better view than mine. Let’s dig into it. Thankfully, and I respect them for this and wish more scholars did it, they provide principles underlying their argument.

Their Principles

Principle 2 is that any valuation be a clearly defined dollar value. I completely agree. A dollar value has to be created if you want to use it for corporate valuation, but I’d also say this requirement is central for most uses of the idea, e.g., setting managerial customer strategy.

Principle 1 is where I disagree. (I’ll explain why after I show the consequences of their choice).

First, if it is indeed the case that resource allocation decisions should in general be made to maximize CE, and that maximizing CE should maximize SHV [shareholder value] as well, then the best definition of CE should be one that its brings its level as close as possible to SHV.

McCarthy and Pereda, 2020, page 6.

Future Customers And Customer Acquisition Costs

They use principle 1 to justify a maximalist view of customer equity (what I’d call the customer asset).

How does their logic go?

They say the value of prospects/future customers matter to the value of the firm. This is absolutely correct.

So they suggest that customer equity has to include the value of the firm’s prospects. Because of principle 1, they want customer equity to include as much as possible that matters to firm value.

A Maximalist View

They say “CLV formulae do not typically deduct CAC [customer acquisition cost]”. McCarthy and Pereda, 2020, page 6. They, correctly, say that if you merge in the value of prospects you must also account for the acquisition costs of prospects somewhere. The authors are also completely right that acquisition costs matter to the value of a firm with growth anticipated (i.e., nearly all firms). They then make a logical leap to say we must define CLV as net of acquisition costs. This is a leap as they could have achieved their aim in different ways. They could have let acquisition costs independently enter customer equity or, better still, enter the company valuation separately for the same effect as subtracting these costs directly from CLV.

Expressing CLV net of acquisition costs they argue solves their valuation problem. In doing so the authors throw retention marketers under the bus. Their CLV can no longer be used for retention. Retention marketers are offered a new unappealing finance term to use, residual lifetime value.

(Using my terms) their maximalist definition of customer equity/customer asset is:

Sum of current customer CLVs + value of prospects – acquisition costs to gain those prospects.

Swallowing A Spider To Catch A Fly

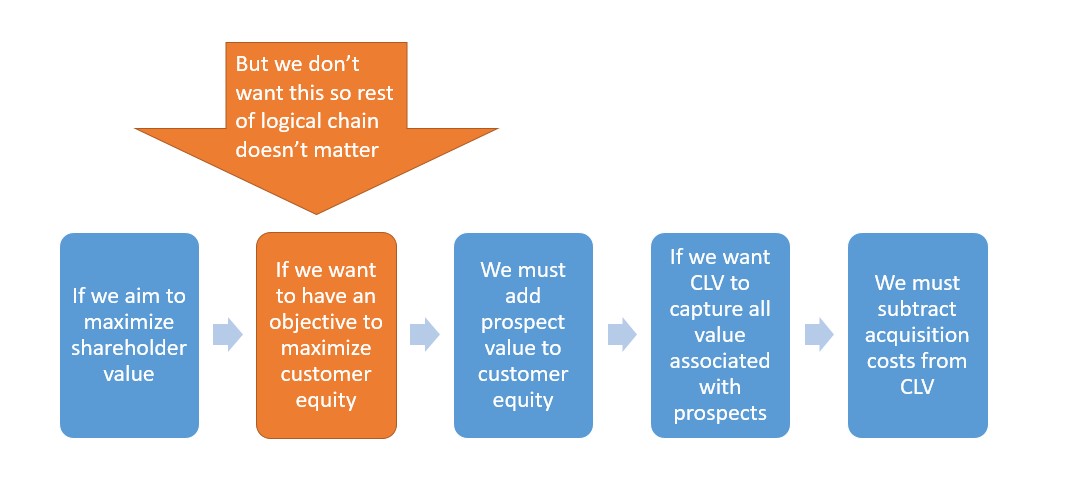

Why I am not convinced by their logic? Their paper starts by, rightly, recognizing that maximizing customer equity is wrong. Yet, the entire logical foundation of principle 1 goes away if you don’t think one should maximize CE. Go back to principle 1 and read it again if you don’t believe me. The point is that you shouldn’t aim to maximize customer equity. They have rightly told us this.

Their first controversial idea to me is the need to incorporate future customers into customer equity. This is driven by the desire for customer equity to be closer to shareholder value. But if you aren’t maximizing customer equity then why try and make customer equity mirror shareholder value? We don’t try and add as much as possible into our measurements of revenue because we don’t think firms should maximize revenue. If we don’t aim to maximize customer equity then we don’t need to make it contain everything important to the value of a firm.

A Second Controversial Idea

Their second controversial idea flows from the first given they have decided to include prospect values in customer equity. Because they claim prospect values are part of customer equity which is the sum of CLVs they leap to the argument that we should subtract acquisition costs from CLV. Again they do this to make the sum of CLVs, which enters customer equity, closer to shareholder value.

The reasons driving their two controversial ideas are based on the logic derived from the idea that one should maximize customer equity. Still, I think, and I’m pretty sure they would agree, that such logic is inappropriate. Basically, principle 1 doesn’t make sense as a starting point. Given that, why follow recommendations derived from applying principle 1?

Where Does It End?

If you aren’t with me yet consider the implications of principle 1. Their logic leads to further problems if you continue to follow it. If something matters to shareholder value, by their logic, you should throw it into customer equity because this will make customer equity closer to shareholder value. Taken to the extreme you should enter things into customer equity regardless of whether they have anything to do with customers. Why not throw in cash balances? Property assets? Anything else you want to put into customer equity? Customer equity becomes shareholder value and shareholder value becomes customer equity. (It feels like a crossword puzzle. Confusing and a bit of a waste of time).

Don’t Maximize Customer Equity

Isn’t it just easier to stick with, what I took as, their initial suggestion? Don’t maximize customer equity. This seems like great advice. You can still use a measure of the value of the customer base (the customer asset), a prediction of the value of prospects, and what it’ll cost to acquire those prospects in your company valuations.

A bonus is that if you aim to measure the customer asset, rather than maximize customer equity, you can do that without having to take a stand on the controversial issue of corporate purpose. An asset’s value is what it is regardless of your position on the rights of shareholders versus stakeholders.

The advantage we have if we take a minimalist view of the customer asset is that we can clearly define it. Amongst other things, I think we can do a better job following principle 2 — giving a better definition — if we ditch the inappropriate principle 1. We can then agree that the customer asset is important to many (probably all) firms. Still, the aim of the firm is not to maximize the customer asset. Simple.

Read: Daniel McCarthy and Fernando Pereda (2020), Assessing the Role of Customer Equity in Corporate Valuation: A Review and a Path Forward. Date Written: January 14, 2020, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3518772, Posted: 7 Feb 2020