You don’t have to be in marketing long to realize that the way financial accounting treats it doesn’t inspire much confidence. This is a topic I have noted a number of times in my blog, for example here, here and here. For this problem we have a solution, Marketing Accounts.

Read Our Marketing Accounts Paper For Free

Xin Wang and I outlined the full argument for changing the way accounting for the work of marketers in a research paper. We published this in the International Journal of Research in Marketing a few years back. We called the article Marketing Accounts. I’m pleased to say that the full text of this research article is available free of charge here. (We would like to thank SSHRC/the Canadian government for this as they provided the funding).

Financial Accounts Often Miss The Value Marketing Creates

Marketing investments not being recorded as such creates a major problem. We have noticed that research in marketing that tackles this issue often proposes a simple solution. The instruction marketers give is that financial accountants should change the way they do their jobs. While I have no problem with this recommendation it may be forever before the change occurs.

The challenge is that marketers and customers suffer most from the problems that not recoding marketing assets creates. It is not financial accountants that suffer. Perhaps, given this, it is less than surprising that accountants are generally not rushing to embracing change.

Marketing actions frequently create long-term value yet this is often not recorded in financial accounts”

Bendle and Wang, 2017, page 1

Markets Can Do Better Without Financial Accounting Change

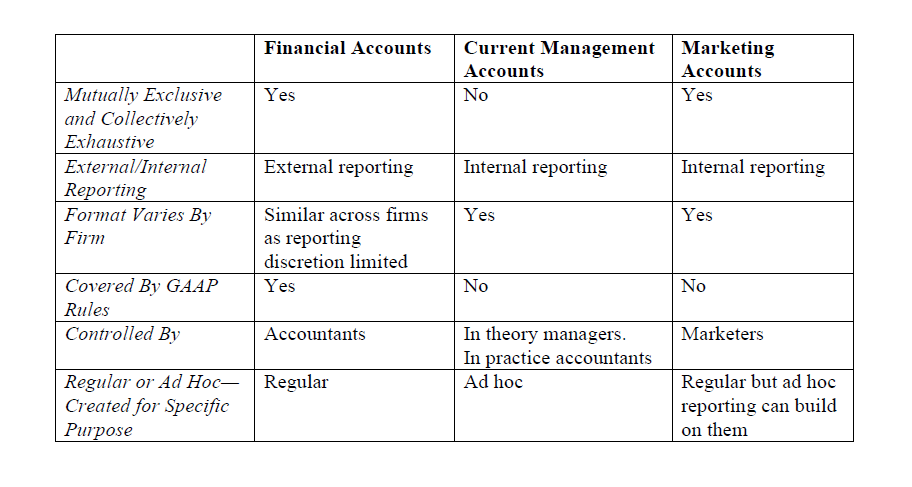

Our suggestion is better internal accounting for marketing. We argue that marketers should take control of a set of management accounts. The marketers can then make them useful for marketing managers.

I would note that management accounts are already supposed to be useful to managers. Sadly, management accounts often aren’t that useful to managers. This is because internal reports typically follow external reporting rules). To help marketers drive the change we outline principles of internal “Marketing Accounts”. We show how these principles differ from current accounting practice.

“Marketing accounts capture the value of market-based assets, applying accounting’s matching concept as consistently as possible to treat marketing as an investment where appropriate.”

Bendle and Wang, 2017, page 1

Differences Between Financial And Marketing Accounts

There is one key difference between financial and marketing accounts that it is worth highlighting. The matching principle from accounting applies consistently. Doing this makes what we propose quite different to current practice in financial accounting. We believe that if a marketing investment creates a marketing asset, then this asset’s value should be accounted for. (Contrast this with current general approach in financial accounting is to largely ignore investments in marketing).

Double Entry

Marketing Accounts borrow the idea of double-entry bookkeeping. This is an excellent invention as it gives reassurance that everything adds up. Consider that to add an item you need to be able to show what the other side of the transaction is. For example, if you add revenue you need to show an asset being built up. This might be a debtor who owes you money or cash in the bank. As a result of the innovation of double-entry an auditor can check if you really have items to back up the revenue reported. Of course, this won’t be perfect. But if you claim an growing brand value you have to account for the strong brand somewhere. The marketer will at least have to muster, and record, evidence for their assumptions. Marketing accounts help create accountability by getting things on record.

Accounting Principles

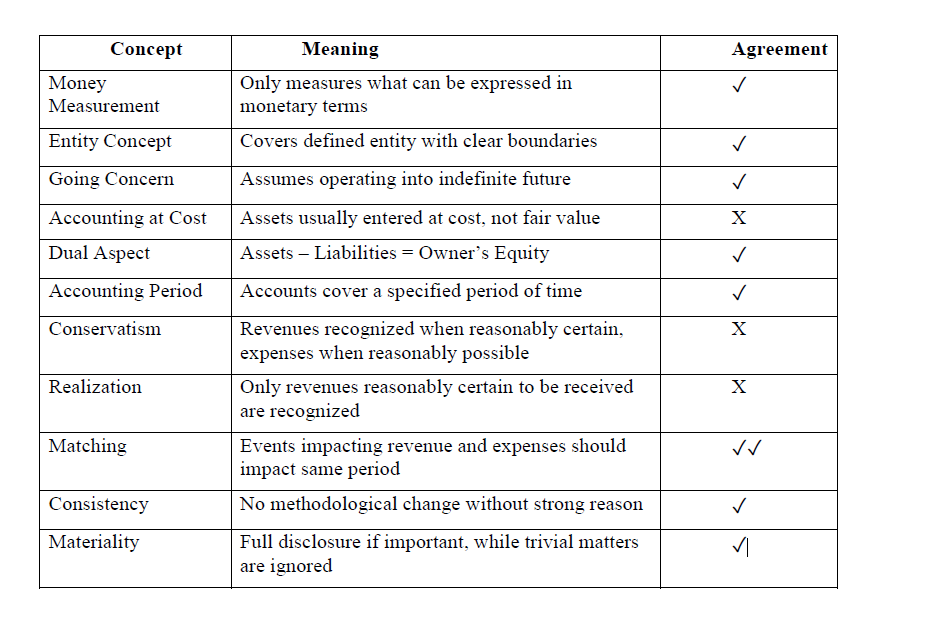

No single set of accounting principles covers all accounting. As such, we took some from a text book to outline differences. We highlighted where there is agreement between what a marketer would want and current accounting practice. Many accounting ideas would stay the same — e.g., the entity principle. Accounts should after all cover a well-defined grouping. Consistency and going concern matter in all accounts.

Our advice is to base accounts on expected value. This means forsaking the principles of conservatism and realization. Marketing accounts aim for ‘true values’. I would say that financial accounting currently takes a ‘what should we tell the children’ approach. What accountants say sometimes has a connection to what they think but very heavily edited for social acceptability.

Another principle we throw out is accounting at cost. This principle lacks any significant theoretical basis. Marketers should justify the entries they make. They should not hark back to an irrelevant historic value.

Change Can Happen Now

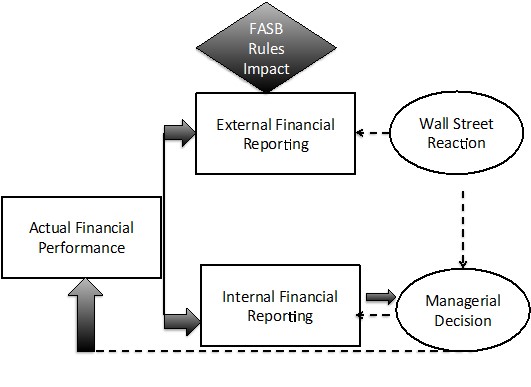

Marketers cannot unilaterally change financial accounting rules. Yet, they can create formal systems to record all firm assets — marketing accounts — today. Marketers can change the way marketing is accounted for internally. After we change the way marketing investments are reported you still might not be doing well. Still, at least the score will be fair.

To repeat: Because this change is about managerial reporting it can happen today. financial accounting GAAP has no remit over internal reporting. Why not read our paper and set up your own set of Marketing Accounts today?