Think of a brilliant move in soccer. The player shows great vision, and excellent passing. There is some fantastic build up play where lots of people are involved. The movement shows amazing promise and then someone slips and blasts the ball miles away from the goal. To my mind that is where we are in the field of customer reporting. Specifically today I will talk about Customer Equity Statements

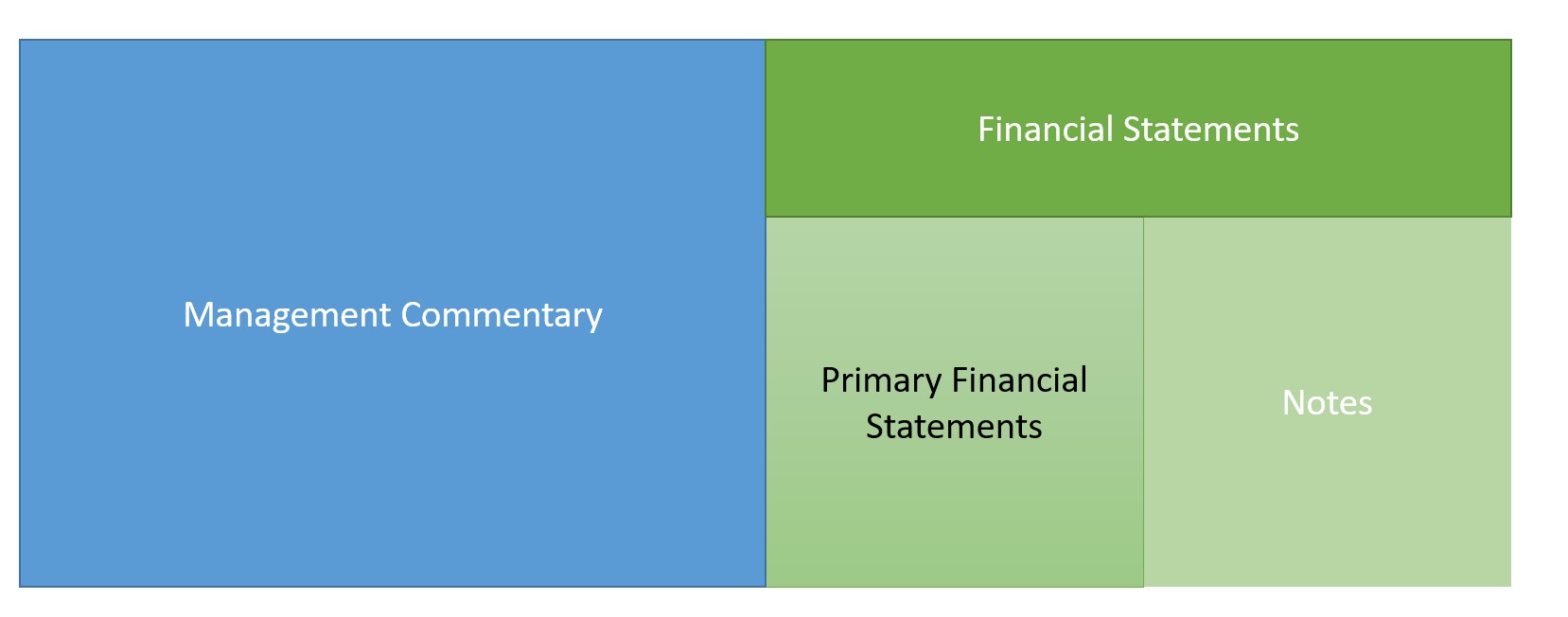

The Vital Role Of Management Commentary

Thorsten Wiesel, Bernd Skiera, and Julián Villanueva had a really powerful insight that underlines their 2008 piece on customer equity statements. Too much of the time marketers don’t really know what they are asking for in respect of customer reporting. As such the requests are all very vague. ‘Financial accountants should do something’. No one is sure what exactly but marketers all agree that what is happening currently isn’t good enough.

The authors rightly saw the problem and they wanted to be much more specific. They noted the challenge of getting items onto the balance sheet. This powerful insight lead them to argue that there is a much less fraught way of making progress than searching for elusive balance sheet recognition. (Balance sheet recognition would be if customer relationship values were added to a firm’s asset’s book value). Firms disclose customer information anyhow so why not make it more meaningful? There is even a great spot for the new meaningful metrics to go. Why not add it to the Management Commentary? (They are Europeans and use the international (IASB) terminology, think Management Discussion And Analysis if you are in the US).

The idea to bring greater detail on customers to the management commentary is powerful. The authors even outline a few reasons why more detail would be helpful. Marketers, and fair-minded accountants, can surely rally behind such a claim.

Customer Equity Statements: A Great General Idea

The authors, therefore, outline what is needed for financial reporting information to be appealing to those who deal with the reports. To tell us more about the value of customers the authors have an idea for a set of statements to do this. They are even very clear about what their work is not.

Note that we discuss an accounting measure of customer base value that can be used not in the primary statements (i.e., balance sheets) but rather in a supplementary section with financial reports..

Wiesel. Skiera, and Villanueva (2008) page 1, footnote 1

I appreciate that they are very clear about what it is not for. I have seen marketers misunderstand this point but authors do not seek to change book values — what is reported on the primary financial statements. The authors have done everything they can to avoid confusion on usage. Readers, I think, have made mistakes interpreting the advice of this paper but that is on the reader. The authors clearly are all about the management commentary.

Wiesel and his colleagues even outline a clear illustrative example using Berger and Nasr’s (1998) simple and effective early approach. So far, so great. I am really impressed by this work, let me say. I will return to the soccer example, the ball has been skillfully maneuvered into the penalty box and all that is required is the final tap-in.

Things Fall Apart (A Little Bit)

To mix a metaphor then things start to come off the rails. The authors lay out a customer equity statement based upon Netflix data. This company is an unfortunate example as a key element of CLV is retention spend. (Customer equity is typically said to be the sum of the CLVs of the firm’s customers.) Sadly, Netflix claims it doesn’t do any retention spend. I understand the author’s problem — getting data is always a challenge. Still, it does limit the appeal of the example when three of the seven main reported items are blank because no retention spend is reported.

They also define customers brought forward from the prior period as “existing” customers. This is a problem given a bunch of them are lost in the period and so don’t exist at the end of the period. This is confusing if you are skimming it but if you follow the math you can see what they did. It is just a case of strange terminology.

Customer Equity Statement

The terms aren’t the real problem. In the Netflix example, the authors seek to operationalize Customer Equity as the sum of CLVs after marketing expenditure. They tell us in a line covering pages 7 and 8 that this value is net of retention costs for existing customers and net of retention and acquisition costs for new customers. (The definition of ‘new’ is customers recruited in the period that is being discussed). The obvious question is why the difference in the formula?

I have written extensively on the fact that if you subtract a sunk value (acquisition costs of an already acquired customer) from a forward-looking measure you get something that simply doesn’t make sense. I believe the authors saw this problem for “existing” customers, i.e., those brought forward from the prior period. For these, they used a calculation that makes sense. (They could after all have tried to subtract acquisition costs from these too. Maybe lack of data hindered them and they were reluctant to subtract current acquisition costs from customers acquired a while back).

Yet, the problem is essentially the same for the new customers — those recruited this year. Subtracting acquisition costs means that the figure calculated does not represent a customer asset. This is despite monitoring assets being an aim of customer equity statements mentioned in the abstract.

What Does It Mean?

The authors say they want to use “forward-looking customer metrics” (noted in the abstract) but they don’t. Part of the confusion arises because the nature of the statement itself is somewhat confusing. A statement of value has to be at a specific point in time. I own $100 today, tomorrow I might own $120. The values are specific to the exact time. Still, the customer equity statement vaguely refers to a ‘quarter’, i.e. three months.

I think the statement has to clearly be written as at the end of the quarter that they refer to. In this case, the acquisition costs of the “new” customers are already sunk. The value of the current customer base is simply not impacted by past acquisition spending even if the past is relatively recent. The value is at a specific time yet the customer equity statement is vague about what time exactly that is and merges a bunch of stuff together.

The authors combine some sort of measure of the future value of ‘existing’ customers with something trying to assess the value of the ‘new’ customers. The value of new customers is assessed over the entire span from prior to their acquisition to the end of the customer relationship. What does this combined value mean exactly? Maybe I am being dense but I do not know.

It is certainly not, as claimed, “the value of the customer base” (Wiesel. Skiera, and Villanueva, 2008, page 2).

Who Is The Statement For?

Honestly, I have no idea what the statement is designed to do. You might want to look at the value of customer cohorts over time. If you must, netting off historic acquisition costs could show you what cohort you think you made the most money off. Still, you would need data from the beginning of each relationship. This calculation wouldn’t be useful for projecting the future. As the values all change over time why would you include long-forgotten values in your projections? This measure certainly wouldn’t be an asset valuation but it would be a consistent calculation. (If a bit useless).

At the moment I don’t know what the statement means and who is asking for it? As such, I think it is going to be very hard to persuade financial accountants to use this. It means nothing to me. I think it will mean nothing to CFOs. It is confusing for investors too.

Why can’t we just lay out a clear statement of what we think the customer asset is? Accountants might go for that.

Customer Equity Flow Statement

The authors add a customer equity flow statement. This shows changes over the period. (Think of this as closer to a P&L statement for customers and the customer equity statement as closer to a balance sheet including extra between period reconciliations). The problem I have is that I don’t really know what the customer equity statement means. Given this what the changes in the customer equity statement mean are even harder to interpret.

Great Potential Remains

The reporting of customer base metrics, including some sort of valuation, has great potential to my mind. The authors made a truly significant contribution and I do value this paper. Still, to push this field further marketers need to be absolutely clear about what we are doing. Remember the values of assets are at a specific point in time. Any forward-looking metric can ignore anything that happens before this time.

For more on CLV see here.

Read: Thorsten Wiesel, Bernd Skiera, and Julián Villanueva (2008) Customer Equity: An Integral Part of Financial Reporting, Journal of Marketing. 2008;72(2):1-14. doi:10.1509/jmkg.72.2.1