Customer centricity is a very good book. It is short and has an excellent point. You could read it in a long bath despite there being much to learn from it. So what then can we learn about customer centricity and customer equity from Peter Fader’s book?

A Strong Start And Clear View Of Customer Centricity

One of the strongest parts of the book is the start (and its refrain at the end). This tells the classic story of Nordstrom taking back tires that the retailer did not sell. Indeed, the retailer did not sell any tires. This is fabulous customer service but it is not what Fader defines as customer centricity. The great customer service was an example of the customer always being right but it was not about focusing on the right customers. As Fader says, customer centricity is about recognizing that all customers aren’t equally valuable. You find who the right customers are and focus, nearly all of, your resources on these best customers. The other customers aren’t the focus. There is no need to fire them but don’t pamper them either.

The logic is hard to argue with in respect of a for-profit firm. Obviously, if you are running the organization under a public mandate, e.g., a utility, the calculus will be different. Still, absent an overriding public interest or similar concern, if it isn’t profitable to serve a customer given your business model then don’t lavish resources on them.

Customer centricity requires in-depth knowledge of the customer. That is why the companies he talks about as customer centric are serious about their customer data, e.g., Tesco. The concept is well explained and the motivation towards organizational change is very strong.

Customer Centricity And Customer Equity

I appreciate Fader’s work to make sure that the idea of customer centricity is clear and well understood. He wants the same thing to happen for customer equity. Here I think his intention is spot-on but it doesn’t really work as well. First the admirable intentions:

… it bothers me when people talk about customer equity as some sort of hazy indefinable concept because customer equity is anything but hazy or indefinable.

Fader, 2012, page 61

I agree that marketers need to be very clear about their ideas. The idea behind CLV is that you can put a hard number on the value of a customer. This should not be hazy or indefinable if the idea is to be accepted and widely applied.

The Challenges

Fader may be inadvertently causing some of the challenges we see with lack of clarity about measures.

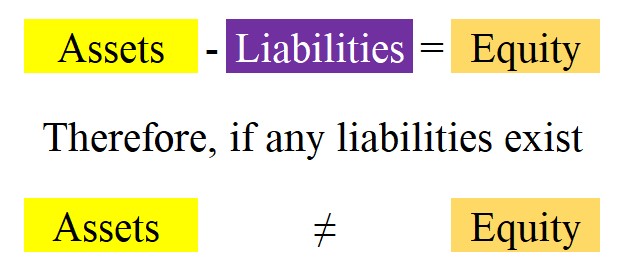

Talk to a traditionalist…and you’ll likely hear that a firm’s total equity can be derived by adding up all the assets, tangible and otherwise, that can be found in one of two equity silos.

…. Add the two together and there you have it: a company’s total equity.

It is hard to argue with this methodology, of course.

Fader, 2012, page 58

Consider the accounting equation: assets minus liabilities equals equity. This clearly implies that assets and equity are different things. If you add up subsets of assets you simply misname assets if you call them equity. (Even in the implausible situation that you have no liabilities then assets still aren’t conceptually the same as equity even when the dollar values are the same). If you then add up all the assets together this does not make them total equity.

This traditionalist’s view is wrong and I don’t mean wrong from the marketer’s perspective. Although I do agree with Fader, here I am not arguing, as he does, that the traditionalist forgets customers or brands. I mean the traditionalist, as portrayed by Fader, is just wrong. Fader thus plans to modify an incorrect view by adding in customer equity. (I’m not a fan of the term customer equity either BTW — see more here). Following Fader’s approach the traditionalist’s view of the firm’s assets will still be wrong but ****now with added customer equity****.

Acquisition Costs, Again

Here is my regular complaint about CLV and customer acquisition costs. (For more on CLV see here). Fader wants CLV not to be hazy or indefinable. He says it is essential to use only relevant data — so far so good. But then says:

For instance, although a proper calculation of CLV must take into account customer acquisition costs, only the most directly applicable of those costs should be considered.

Fader, 2012, pages 73-4, my italics

The idea that to be ‘proper’ CLV must take into account acquisition costs does not work for me. Given only relevant costs should be considered and acquisition costs are only relevant prior to acquisition logically, at best, Fader implies that CLV can only be ‘proper’ if predicted prior to the customer being acquired. This means CLV can only be used for marketing decisions when the prospect you are focusing on acquiring is not yet a customer. I think this is problematic — it abandons many current CLV uses and strains the English language to breaking point in that customer lifetime value doesn’t apply to customers. That said, it is certainly logical.

Yet, Fader argues that CLV can be used for retention/development decisions just a few lines before.

…how much money we should be willing to spend to keep [the customer]. In a sense, this is what CLV gives us.

Fader, 2012, page 73

Logically this could mean CLV can only be used for retention planning prior to acquisition. Still, we then need to know what to do with planning for retention after acquisition. Surely we need CLV to help with decisions about current customers if it is to be the basis of a complete customer strategy?

Customer Heterogeneity

One of Fader’s main contributions is that he argues, very skillfully, that assumptions of constant retention rates are likely wrong. He makes a great — clear but not immediately obvious — point. Customers likely have different propensities to stay with your firm. Those who are more likely to churn (cease to be retained) in any period by the laws of probability are more likely to churn in the earlier periods. Thus, we are likely to see sorting, customers with a better-fit stay. This means customer retention rates are likely to increase over time. Customers that stay for a while have stayed for a reason and so are more likely to stay going forward than a new customer.

To conclude, given it is so valuable I don’t want to lose the message of the book. Customer centricity is an important concept. Fader explains it very well. It is not about being nice to customers, but about focusing on the right customers.

For more on treating customers as assets see here, here, here, here, and here.

Read: Peter Fader (2012) Customer Centricity: Focus on the Right Customers for Strategic Advantage, Wharton Executive Essentials