I think the idea of using customer information in corporate valuation is a great one. As such, I am very receptive to work on customer-based corporate valuation. A 2005 paper in Management Decision I think well illustrates some of the challenges I have seen in this field. Lots of good ideas, some reasonable points, but also many strong debatable statements that aren’t properly theoretically justified. They also want to be cross-disciplinary without thinking through the challenges.

Cross-Disciplinary Research is Hard

The classic problem here is that the authors want to speak to accountants but don’t seem to understand accounting. To be fair cross-disciplinary research is challenging by its nature. Not only do you have to try and understand your field but you have to understand other fields. You can see why many scholars take the option of zeroing in on a narrow field and becoming an expert on something so small it descends into pointlessness. Narrow is much safer so let’s first commend the author’s ambition.

It is to Bauer and Hammerschmidt’s credit that they are clear in their cross-disciplinary ambitions.

According to our research objectives, the paper is targeted at accountants and auditors, as well as business analysts who undertake valuations for market floatation or M&A of large corporations.

Bauer and Hammerschmidt, 2005, page 333

Unfortunately, the idea they advance is deeply problematic for the aims they set themselves. A challenge here is that valuation for determining corporate value for mergers and acquisitions (which takes more of a ‘what works is good approach’) seems very different to valuation in accounting. Financial accounting valuations, especially in US, are much more rule-based. To be clear the process doesn’t really aim for a true value. Still, it is one thing to try and talk to financial accountants but the authors want to go further and talk to auditors. Auditors are the police of accounting. They think accountants are wild people who take loads of extravagant chances. As such, it is hard to imagine what auditor they thought would find their work convincing given I see it as much more pitched towards more free-wheeling finance people.

CLV As A Catch-All Concept For Customer-Based Corporate Valuation

The authors argue that CLV has to include pretty much anything that someone might care about in a customer-based corporate valuation. The points covered are all generally reasonable ones. I agree that word of mouth does matter to the future value of a firm. Acquisition costs do matter going forward when you are looking at the value you can gain from prospects (future customers). The problem is that adding everything to CLV means it becomes a messy, massively subjective metric. What do auditors really hate? Messy, massively subjective metrics,

On word of mouth (referral value) they give a model that provides a number. This may be good enough for external valuation but it would make any self-respecting auditor sit in the corner and cry. (I shed a little tear and haven’t done any auditing since the mid-90s.)

Current And Future Customers

The authors explain that they must include current and future customers in customer equity. They say:

With these models [that don’t capture future customers] a shrinking customer base over time is therefore implicitly assumed, resulting in an ultimate customer base of zero. Thus…”

Bauer and Hammerschmidt, 2005, page 338

My problem here is with the use of ‘thus’. It is a complaint I commonly have with writing. The authors make a reasonable statement and follow it with ‘thus’. Unfortunately, the next sentence is not logically implied by what came before the ‘thus’. We can talk about what they want to do but they need to give more than a ‘thus’ to justify it. The random ‘thus’ is one of my greatest complaints with academic work. Thus, after all, implies what follows is justified by what came before. When I read papers usually ‘thus’ means that the authors are going to make a massive logical leap and hope no one notices.

My Usual Plea On Acquisition Costs

I especially liked their justification for subtracting acquisition costs before reporting CLV. Let me say first, so it is very clear, that you should absolutely consider future acquisition costs when looking at customer-based corporate valuation whenever you consider any future customers. I am not against that in any way. What I worry about is mixing everything into CLV as it leads to confusion.

Still, perhaps they gave a compelling argument for generating confusion. Here it is:

Although for existing customers, they [Acquisition costs] are no longer relevant for marketing decisions and have to be booked as sunk costs they should be incorporated in the calculation of CLV for the purpose of company valuation.

Bauer and Hammerschmidt, 2005, page 335

They then mumble something about net value. This does not explain why they need to have acquisition costs in CLV. Basically, they forgot to put a reason into the paper. They just gave a reason not to do what they do with acquisition costs elsewhere and said this is a different situation. Why is it different? Given the exception is for marketing decisions should you also subtract acquisition costs from CLV for current customers in valuation? Why would this create a valuation of anything?

To illustrate the problem with their logic if I tell my kids not to run with scissors in the house this does not imply I’m recommending that they run with scissors whenever they are in the garden.

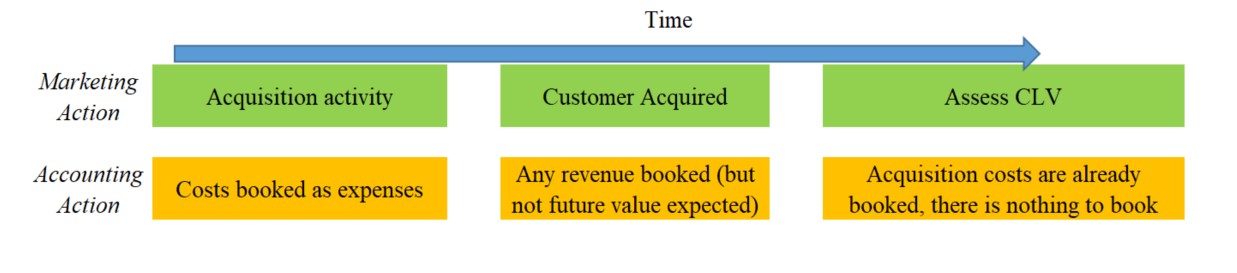

Booking Sunk Costs

Look again at the explanation. They say that acquisition costs “…have to be booked as sunk costs”. Expenses (as acquisition costs are treated) in accounting terminology will be booked when they are incurred. This ensures that by the time any expenses are sunk they are already “booked”. As such you should never book a sunk cost.

To be clear sunk costs are irrelevant so in decision-making theory you don’t consider them, you ignore them. In accounting, you do book things so that sounds more plausible. Yet in accounting you don’t book things that are sunk and therefore will have already been booked. This is a weird mishmash of two approaches, accounting and decision making, which makes sense in neither. (I say this with confidence. I am an accountant whose Ph.D. focused on decision-making).

If you are interested in decision-making you may be thinking sunk costs are considered by people in error. I agree. Yet, people consider sunk costs usually because those making the error miss the fact they are sunk. (Maybe including these authors). It is not because the costs are ‘booked as sunk’. Booking a sunk cost doesn’t make sense in mental accounting either — an approach primarily concerned with budget allocation. (Budget here is in its widest sense including your personal time).

Customer-based corporate valuation has lots of potential. The authors did us a favor by advancing the field but there are some pretty obvious problems in the work.

For more on Customer Lifetime Value (CLV) see here and on customer equity see here.

Read: Hans H. Bauer and Maik Hammerschmidt. “Customer‐based corporate valuation.” Management Decision (2005).