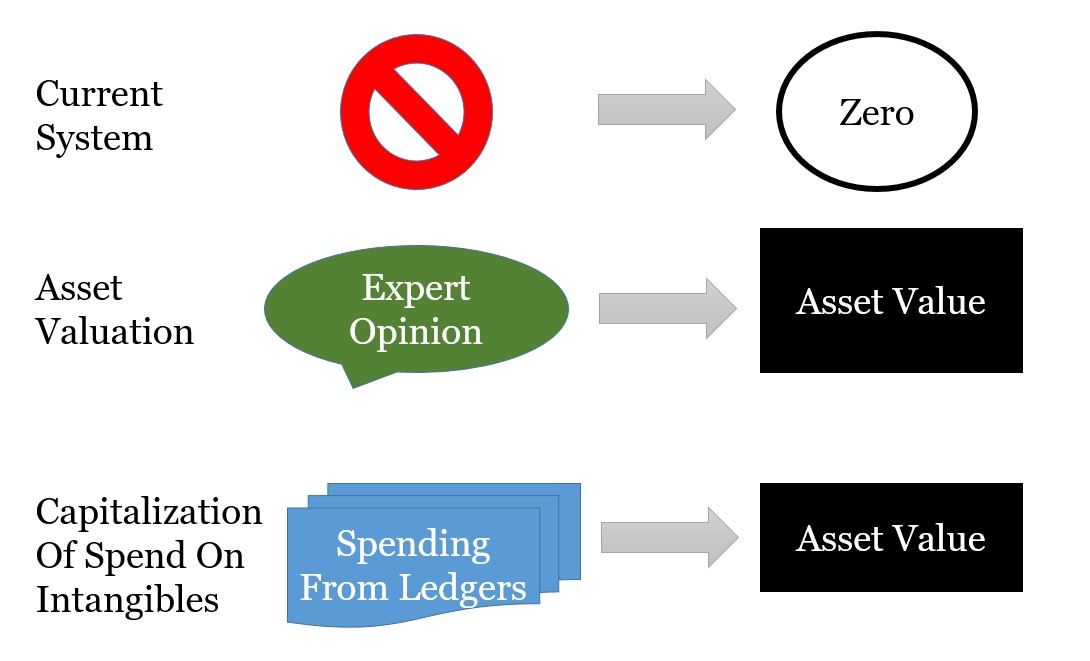

My final comment on Lev and Gu’s The End of Accounting discusses their idea of how to improve financial reporting. This is a bit more controversial to my mind but worth considering. They suggest capitalizing spending on intangibles.

Too Many Estimates?

The authors argue that accounting uses too many estimates. As such, although the authors want to create more records of intangibles they argue against adding estimates onto the balance sheet for brand values and other intangibles. (This is because the fair values of brands and other intangibles are extremely hard to come up with.) Instead, they offer the suggestion that objective values should be used.

We don’t suggest to value intangibles by their current purchase or sale prices (fair values). Rather, in line with the treatment of these assets in the national income accounts, we propose to capitalize the investment in these intangibles, using their objective original costs.

Lev and Gu, 2016, page 215

Capitalizing Spending On Intangibles

The argument is that capitalizing spending gives an objective value. What was actually spend is a number we have verification of. To capitalize a brand asset we use the records we have of what was spent on brand building. The advantage is that managers and their auditors can’t just pick their favorite valuation system. The downside is that the amount spent may not have too much connection to the value created. (This is a significant concern in my mind).

Maybe capitalizing investments in intangibles is not going solve all the problems we see. That said, it may be acceptable to accountants and so this may make it worth thinking about. (At least as a short-term fix).

For more on accounting for intangibles see here, here, and here

Read: Baruch Lev and Feng Gu (2016) The End of Accounting and the Path Forward for Investors and Managers, Wiley