Tony Tollington’s book on Brand Assets is fascinating. The book is not an especially easy read. Indeed, it gets into some pretty detailed philosophical debates around the nature of assets and accounting which can be tough. That said it is good to think about these things and Tollington definitely made me think. There is a signiificant problem looking at goodwill and marketing.

Goodwill: What Is It?

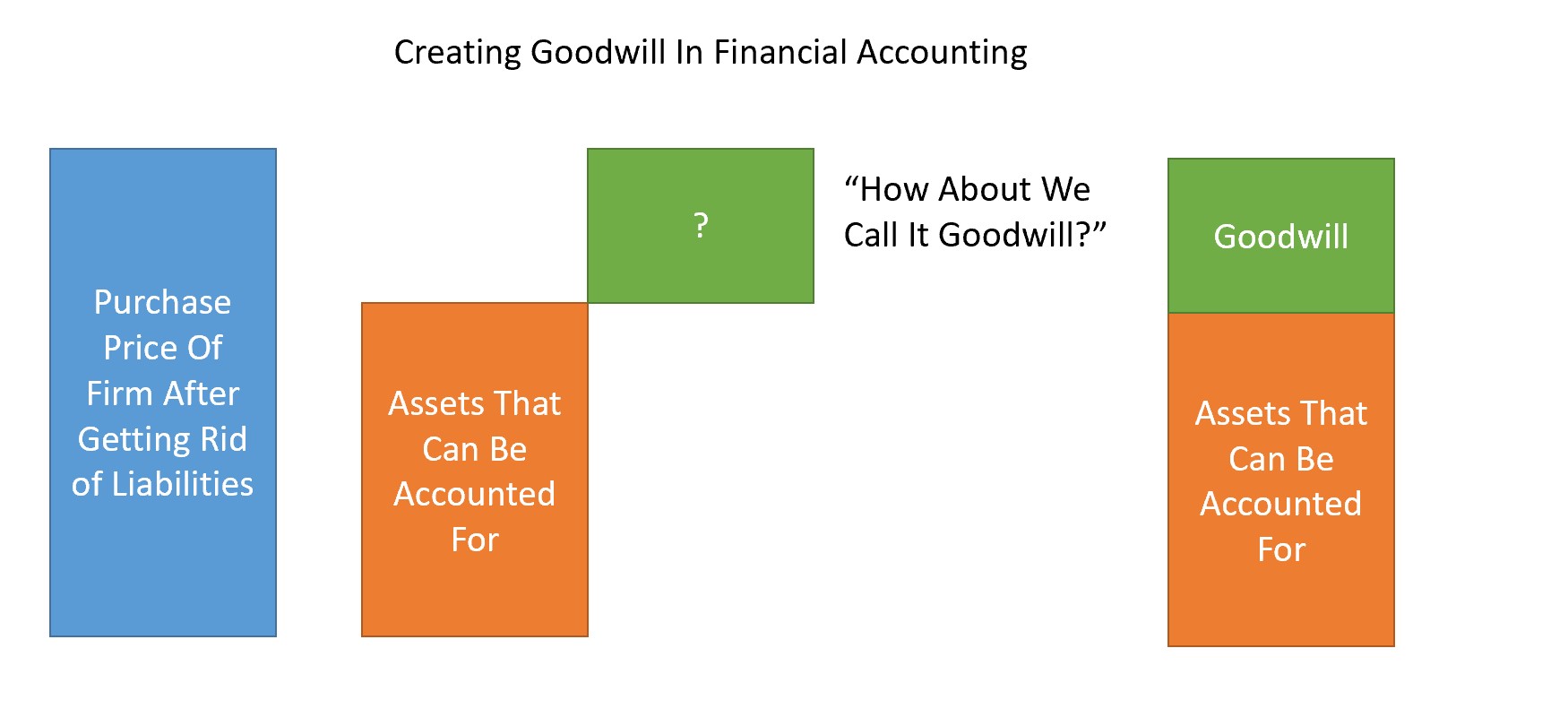

One key thing he discusses is the idea of goodwill. Goodwill appears on company balance sheets as part of assets. It emerges from the difference between the recorded assets of a purchased firm and the amount the purchasing firm paid. The idea is that the firm doing the buying must have bought something. The recorded assets of the purchased firm aren’t enough to justify the price paid so, voila, goodwill.

“If anyone asks what goodwill is, accountants can point to a definition which explains that it is a ‘difference'”

Tollington, (2002), page 53

To be honest when I was in accounting I never thought about goodwill too much beyond that. Tollington notes, however, correctly, that this is pretty unsatisfactory. After all a difference is not an asset. Even if one gets over the obvious point that the acquiring company might have overpaid, still assets on the balance sheet are something you should be able to properly describe. A difference is not something to can describe. It is basically an admission you are giving up on describing it. He has an extensive discussion of why goodwill is not an asset. One of the harder to refute arguments is that it would be a problem getting bankers to lend you cash with goodwill as your collateral.

Purchased Goodwill And Marketing

Overall Tollington is not a fan of purchased goodwill. Instead, he argues that we should be more actively recognising actual assets that have historically been subsumed into goodwill.

Things have changed a bit since he wrote so the specifics he argued about are a little different but the general principle remains. That there is a lot of goodwill on accounts and not many brand assets. Tollington suggests “…that whilst brands can be regarded as assets, purchased goodwill is not, by nature, an asset.” (Tollington, 2002, page 81).

For more on financial accounting and marketing see here, here, here and here.

Read: Tony Tollington (2002) Brand Assets, Wiley Finance