There is a lot of work linking marketing and finance. Unfortunately, at least from my perspective, nearly all of this has focused on linking marketing to financial markets. Such work is useful but I would like more looking at more diverse linkages between marketing and accounting. Sidhu and Robert’s article is an exception. They look at the challenges of marketing and financial accounting (external financial reporting) — the marketing-accounting interface.

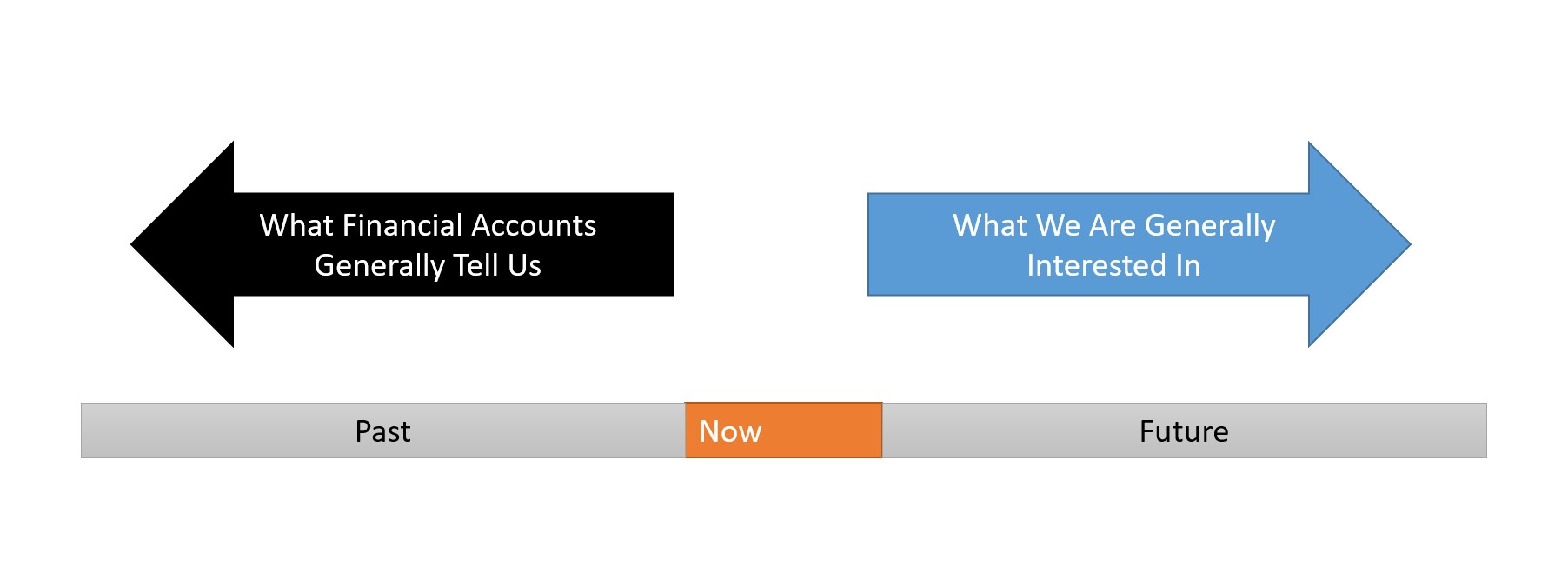

A Focus On The Past

One challenge the author’s note is that:

Much of accounting focuses on the past because the criterion of reliability makes accountant very wary of uncertain promises of cash — and that includes the future to a greater of lesser degree.

“Sidhu and Roberts, 2008, page 672

Telling us what happened, compared to predicting the future, is much easier. Financial statements that do this, i.e. they look backwards, can be signed off on as ‘correct’. After all, we can work out what happened. Although the problem is that sometimes the past is not that useful to know about. While the past can inform the future it doesn’t have to. A stock price might have gone up in the past but there is no guarantee this will continue. A firm might be profitable in the past. Will it be in the future? All previously profitable firms must have had profitable customers in the past. But maybe what worked in the past is no longer working.

The point is that sometimes details about the past aren’t especially useful to anyone in making decisions about the future.

The Marketing-Accounting Interface: Does It Exist In Academia?

The authors give some ideas to help overcome the gap between financial accounting and marketing. They suggest that both look to shareholder value. (I would like a few more details here).

Probably the most notable thing is that what they said about the marketing-accounting interface eleven years ago still seems true to me.

“The most surprising thing about the marketing-accounting dialogue is that there is no dialogue.”

Sidhu and Roberts, 2008, page 676

Sadly this is still true. You might think that there would be a vibrant marketing-accounting interface but it barely exists.

It isn’t exclusively an accounting or a marketing problem but both disciplines are diminished in value by this lack of dialogue. Marketers need to understand how accounting works to influence organizations. Accountants need to understand how business works to make their numbers more relevant. There is a deal to be had there.

For more on accounting for marketing see here, here and here.

Read: Baljit K. Sidhu and John H. Roberts. “The marketing accounting interface–lessons and limitations.” Journal of Marketing Management 24, no. 7-8 (2008): 669-686.