I enjoy a good polemic and Keron Bhattacharya’s book on Accountancy is certainly that. A generation old now but many of the points remain. (Although the acronyms for the UK accounting standards and accounting bodies have all changed). As an accountant himself (member of CIMA) he isn’t very happy with the way accountants were doing their work. What is more he isn’t afraid to say it. What then does he have to say about faulty sums and accounting?

Substance Over Form

Bhattacharya targets the classic “get out” of accounting rules — substance over form. He explains:”…what this rule says is that you must follow the spirit of the Standards and not just the written word. Now if you ask: what is the spirit of a Standard? How will I know it? That is a sixty-four thousand dollar question” Bhattacharya, 1992, page 29).

Accountancy needs wiggle room and this is it. Still, it isn’t very helpful for those trying to understand what is going on.

Consequences Of Accounting Choices: Faulty Sums and Accounting

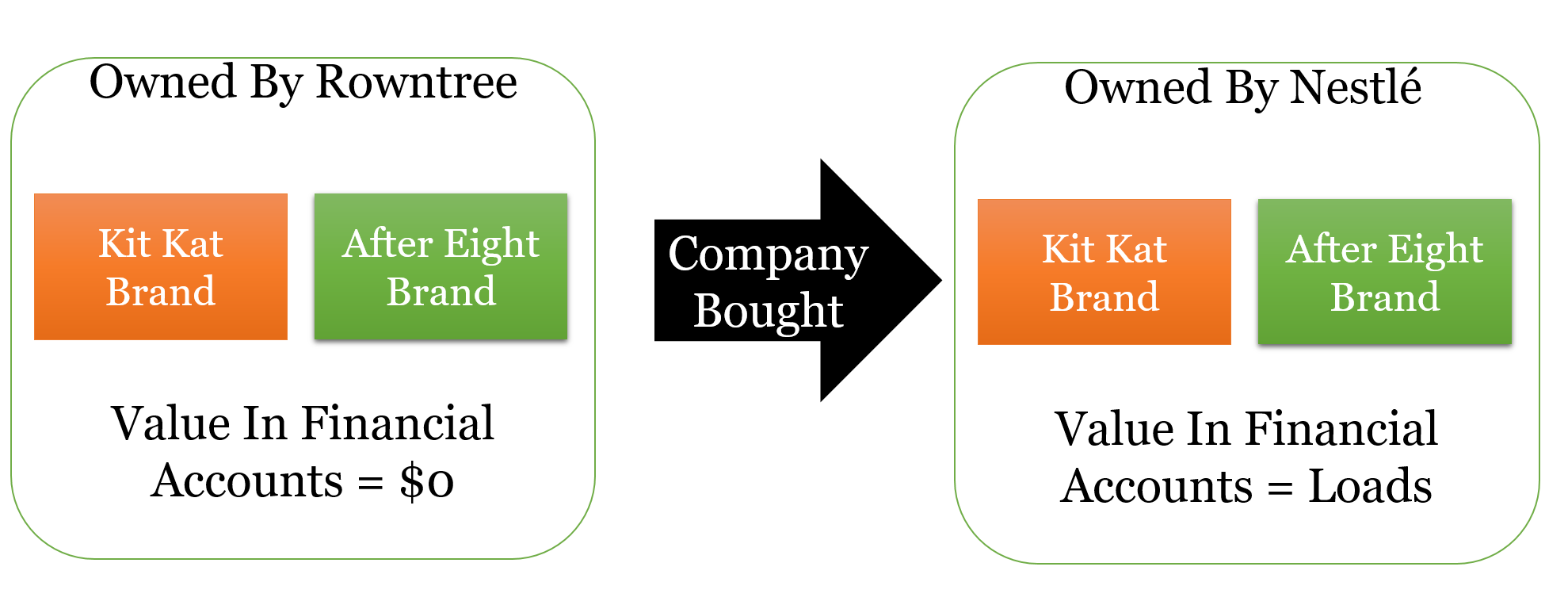

Bhattacharya believes that what accountants do matters. (This is why it is worth bothering to criticize them). He describes the fact that Rowntree, the UK confectionery firm, wasn’t allowed to account for brands such as Kit Kat and After Eight. The firm’s accounts, therefore, made it look not very valuable. He blames this for (Swiss) Nestlé being able to pick up (UK) Rowntree as a bargain. And, of course, because of the peculiarities of accounting rules allowing acquired brands to be added but not internally built brands, Rowntree’s brands could be added to the balance sheet of the Swiss firm after acquisition. This is all, despite the fact, that the brands didn’t really change at all. (For more on Goodwill from acquisitions see here, and on brand valuation see here).

He discusses at length the difference between “extraordinary” and “exceptional” items and how it matters what a firm chooses. He convincingly argues that presentation choices are important despite the general notion that accountants are just straight shooters telling it how it is.

Growth

I liked his comment on growth. Too often I’ve heard marketers discuss growth without really worrying about what is growing. “The question is: What Growth?” (Bhattacharya, 1992, page 156). I agree that growth is only good if it is something you want to increase, profits etc…, not growth for the sake of growth.

Accountancy had a bunch of problems showing it was relevant in the 1990s. A generation on it still does. Hopefully, in a generation time, we won’t be still having the same conversations. We will still be talking about faulty sums and accounting?

For more on accounting for marketing see here, here, and here.

Read: Keron Bhattacharya, 1992, Accountancy’s Faulty Sums, The Macmillan Press Ltd