In a piece for my accounting body (ACCA) I discuss the problem of what to do in respect of brands on the balance sheet. My intention is to help foster a dialogue between (financial) accountants and marketers. I am all about creating discussions between marketers and accountants. A lot of this website speaks to that.

Creating Discussions Between Marketers And Accountants

Too many marketers seem to think accountants are merely there to frustrate marketers’ plans. They may not realize that accounting for marketing is a very challenging activity. Marketers feel cheated by accountants. Yet, often marketers don’t engage in developing a better solution than we currently have.

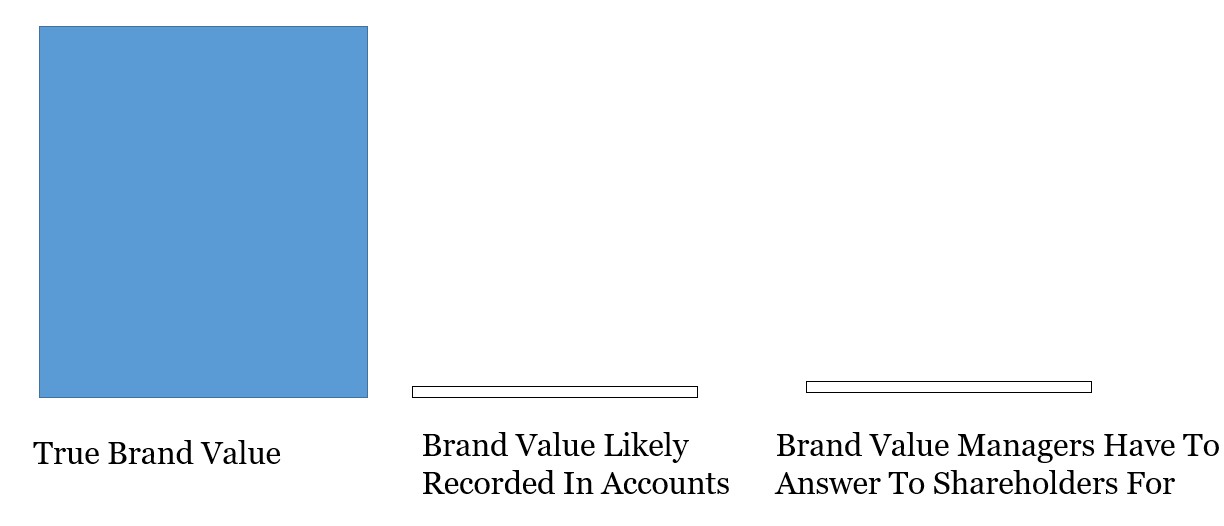

What do we currently have. I will simplify somewhat to give you the general idea. Purchased brands appear on balance sheets at an estimated purchase price. The value of in-house generated brands do not appear at all. Currently, we immediately expense brand building. This treats such long-term marketing the same as short-term marketing).

Marketers are not always reasonable in their requests but they are not alone. Too many accountants imply that accounting rules are set in stone, handed down from some all-knowing source. When a marketer asks whether accounting for brands could be better, “you can’t do that” is not a valid answer. Accounting rules are what they are. Yet, this does not mean we cannot improve on the rules. If we all think about them we can do better. I am optimistic. (Please see the work of MASB, the Marketing Accountability Standards Board).

Accountants Justifying Their Rules

Accountants should be able to meaningfully justify their rules to those who question them. Of course, not everyone will always agree. I see no way to cheer up all sides. Arguments will remain. Still, a minimum should be at least recognizing that the current approach comes with severe problems. Rules can change.

Treating marketing investments as expenses discourages long-term marketing strategies, rewarding instead the short-term gimmicks that give marketers a bad name. Furthermore, unrecorded marketing assets are often abused. Valuable customers are alienated by annoying trick fees. Businesses suffer economic losses as profitable customers vow never to use them again, while financial reports show short-term profits as the fees trickle in.

Bendle, 2017

Hopefully, we can improve the lines of communication with accountants.

For more on accounting for marketing see here, here, and here.

Read: Neil Bendle (2017) The knotty problem of brand valuation, Accounting and Business magazine (International Edition), September